The Wealthiest Bet in the Room

Where's your head at right now? Because billionaires stopped buying yachts years ago — they're now buying time. Not metaphorically. Literally paying for biological age reversal, cellular rejuvenation, and the kind of science that used to exist only in science fiction.

Here is the cloud of fog we're clearing through — two markets going in the same direction and are entirely different animals.

- Anti-aging products (expected to be worth $85B in 2025 and $127B+ in 2031) — aka DTC products like supplements, creams, clinics, and injectables

- Longevity biotech R&D ($30.79B in 2026 and $52.86B by 2035) — aka research-level therapies including epigenetic reprogramming, cellular engineering, and senolytics

The trap door opened. AI drug discovery, genomics, and mRNA all clicked simultaneously. That's not hype — that's a loaded gun sitting on the table.

Here's the Kalyug Capital thesis in a nutshell: longevity moves from underground capital to sector to trade. If you're a trader comfortable hunting alpha in the chaos — 0DTE puts, 3X leveraged ETFs, fine — but the structural money is flowing upstream into life extension biotech before the mainstream arrives.

Here's how the report will unfold: market sizing → catalysts burning in 2026 → five stock deep-dives → ranked table. Let's build the case.

Why Is So Much Money Moving Right Now

So, what's going on in your head right now? Because the richest people on Earth just made a decision, and it's about to ripple down.

AI drug discovery, genomics, and mRNA — three separate technologies — are all ramping up at the same time. Individually, each one might be a trend worth watching. All three simultaneously is a structural shift. And of course, the billionaires got there first.

| Billionaire | Company / Bet | Capital |

|---|---|---|

| Sam Altman | Retro Biosciences (focused on cellular aging) | $180M |

| Peter Thiel | 12 companies including NewLimit, Unity | $700M+ |

| Jeff Bezos | Unity Biotechnology, Altos Labs | Undisclosed |

| Larry Ellison | Longevity plays | $430M+ |

| Brin & Page | Calico Labs | $1B+ |

"Holy crap. It's working! Oh my God, it's actually working!" — Paul Conyngham, after his dog Rosie (with terminal cancer) saw her cancer shrink after a personalized mRNA vaccine trial.

It's a signal — and not an outlier. Take Moderna and Merck's mRNA melanoma vaccine (V940 / mRNA-4157), which saw nearly a 50% reduction in death and recurrence risk over five years. Bryan Johnson's $2M/year biological age reversal program is generating publishable science. You know what the world's wealthiest people aren't paying for anymore? Penthouse views.

The money already moved. You're just catching up now — and the catalysts are burning hard in 2026.

Catalysts Burning in 2026

Money's moved. Now, the catalysts either arrive and justify it — or burn it all down. The FDA doesn't recognize aging as a disease. Price that regulatory fog in now.

- 1. Moderna's mRNA-4157 Phase 3 Readout — In 5 years, it showed a nearly 50% reduction in death and recurrence. The readout reprices mRNA as infrastructure, not pandemic novelty.

- 2. Eli Lilly's Donanemab Rollout — Your grandma's cognitive decline is now a revenue line. Dark. Profitable.

- 3. VITAL-H Trial Launch — Rapamycin plus semaglutide plus dapagliflozin. Seven hundred older adults. First multi-drug aging-marker study. When this data drops, repricing accelerates.

- 4. Ionis' Neurology Calendar — Zilganersen NDA. BIIB080's Alzheimer's/tau data. Independent launches primed. Asymmetry lives here.

- 5. Longevity Biotech IPOs — Retro Biosciences. Altos Labs. When Altman's and Bezos' bets go public, this category will reprice.

All five catalysts share a structural risk: aging itself has no direct FDA path, so while they have plausible age-related condition approvals, none of them are true anti-aging wins themselves. The regulatory fog is real — price it in, don't ignore it.

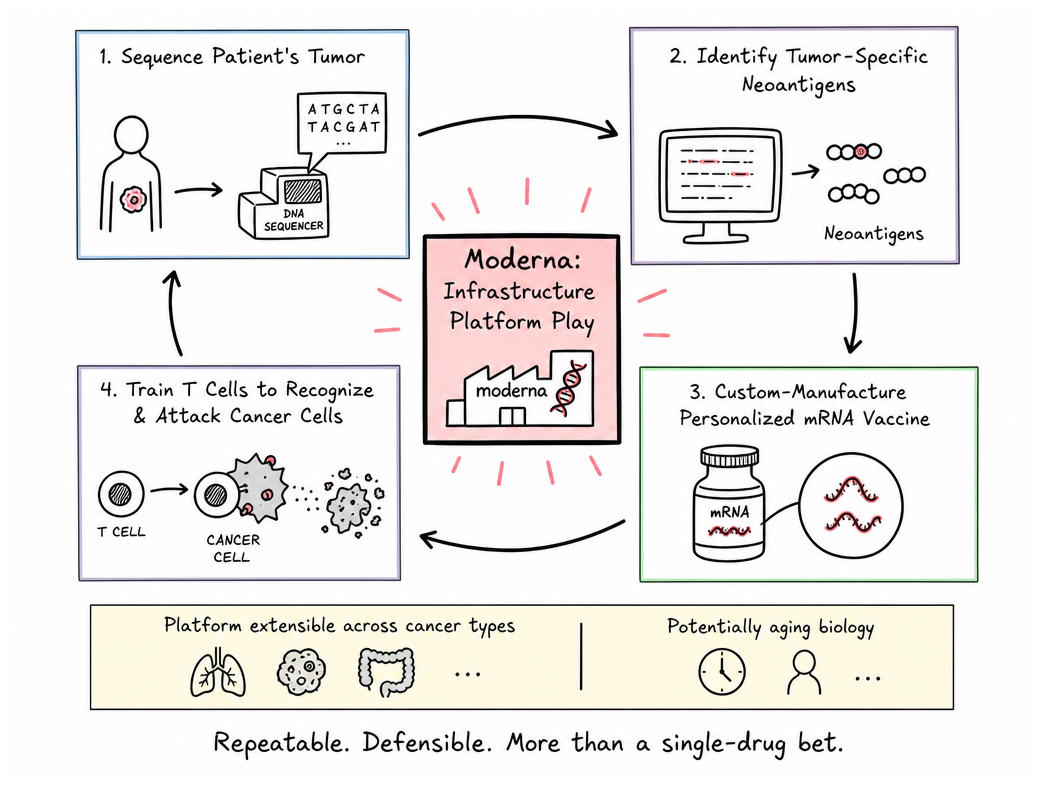

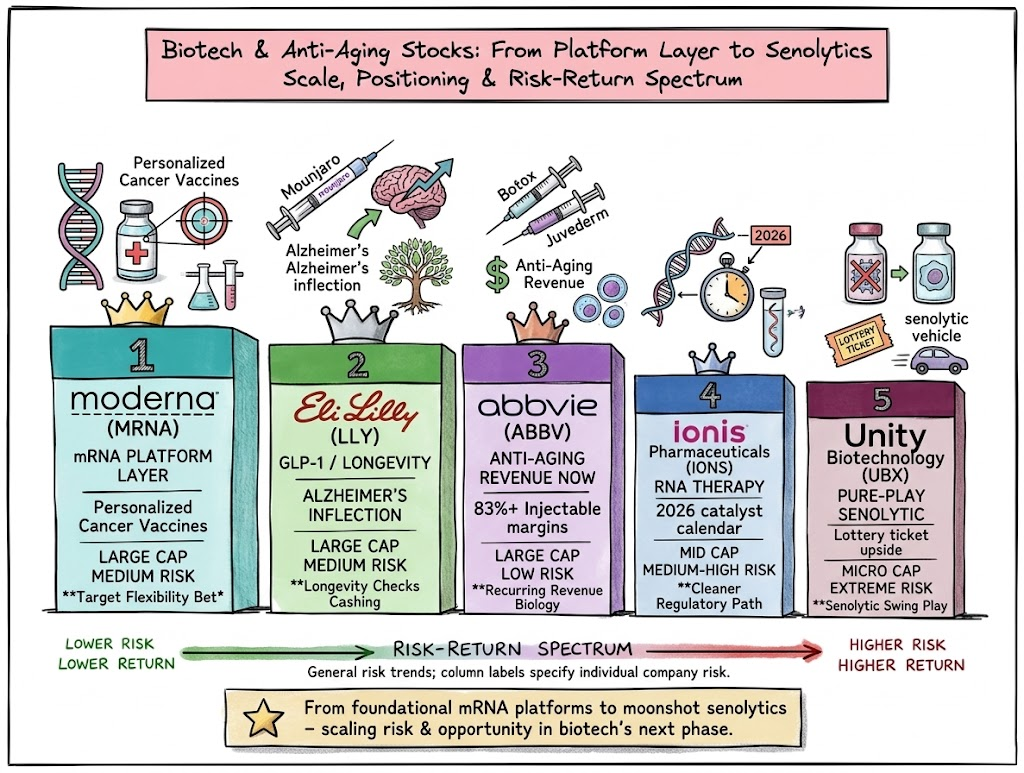

Large-Cap Pick #1 — Moderna (MRNA): The mRNA Infrastructure Play

I haven't heard anybody asking this question loudly enough: what if the vaccine platform that saved millions during a pandemic is actually the skeleton key to life extension itself?

Moderna isn't just another biotech lottery ticket — they're arguably one of the most important companies in the middle of it all. Because they don't see mRNA as a product — they see it as a programmable platform. The same molecular machinery can be repointed at a new target every time.

Over five years, Moderna/Merck's melanoma vaccine (V940 / mRNA-4157) demonstrated nearly a 50% drop in risk of death and recurrence. That's not noise. That's infrastructure. Write it down.

The platform extends beyond oncology. The same mRNA machinery that trains immune cells to kill cancer can, theoretically, address aging-related pathology — tissue regeneration, senescent cell clearance, metabolic reprogramming. The neoantigen logic that works on tumors doesn't care what disease it's pointed at.

Longevity investing isn't for the faint of heart here. Binary trial outcomes mean brutal volatility. Clinical-stage pipeline equals genuine degen territory. You need conviction and a stomach made of iron.

When it comes to personalized medicine, mRNA therapeutics are the deepest moat in the public market. If aging biology bends to the same neoantigen logic that's already shrinking tumors — and it might — Moderna's scaffold becomes the infrastructure the whole ecosystem runs on. High risk. Absurdly high ceiling.

Large-Cap Pick #2 — Eli Lilly (LLY): The Longevity Gateway Drug

Lilly planted itself right at the crossroads where longevity money meets the lookmaxxing flywheel — and that's a crowded, lucrative corner to own.

Right now, Mounjaro (tirzepatide) is pulling in $34 billion in annualized revenue — not some fancy promise or pipeline theater. It's a GLP-1/GIP dual agonist, so the biology is class-leading. Machinery that directly competes with class-defining drugs.

Then there's donanemab — Lilly's Alzheimer's monoclonal antibody now moving through commercial rollout. It's not a prayer but a legitimate revenue line for aging neurodegeneration. Something to take seriously as a commercial catalyst in 2026–2027.

Here's the kicker: Mounjaro's impact on metabolism creates downstream demand for Botox and fillers — the very real "Ozempic face" correction market. Normalizing GLP-1s normalizes the psychological barrier to injectables broadly. That tailwind flows directly into ABBV's aesthetic franchise.

The risks are real — Novo Nordisk competition, pricing pressure, market disruption compounding fast. But LLY's the crossover ticket — not the mRNA moonshot, not the injectable cash cow. The bridge between metabolic medicine and longevity positioning that currently has no peer.

Large-Cap Pick #3 — AbbVie (ABBV): The Anti-Aging Revenue Machine

AbbVie isn't betting on anti-aging. It's already printing it. Not in a pipeline deck. Not in some Phase 3 trial gathering dust. Right now, today, in actual revenue.

Botox Cosmetic at $2.72 billion in 2024. The Juvéderm Collection at $1.18 billion. Running at 83.9% adjusted gross margin — and the business is defensible infrastructure, not a one-time pop.

Why the story matters to the bio-optimized thesis:

- Mass injection normalization collapses the psychological barrier. Once people are comfortable needling themselves for metabolic control, Botox and fillers become natural add-ons — the lookmaxxing-to-longevity flywheel in action.

- Clean Allergan integration. Channel relationships intact. That's execution proof in a biotech wasteland.

- Institutional capital is already positioned. ABBV trades heavy across large-cap biotech funds. That's not hype. That's smart money.

The risk cuts both ways: "Ozempic face" may be both catalyst and threat to the filler industry. Aesthetic procedures are discretionary — the same drug that creates filler demand could simultaneously reduce it if metabolic improvement reduces the perceived need for correction. Price that in.

Best margin profile of the three large caps. Current revenue, not pipeline fantasy. Not waiting for the FDA gods to bless anything. The money's already flowing.

Mid-Cap Pick #4 — Ionis Pharmaceuticals (IONS): The RNA Therapy Underdog

In the mid-cap space, how many biotech companies have two drug launches that are independent from each other and scheduled for 2026? Not many.

While the Moderna mRNA story gets all the headlines, Ionis plays the grittier RNA medicine play: antisense oligonucleotide (ASO). As mega-caps see more mature revenues, Ionis looks to be about to scale from a pipeline company into a launch-stage revenue story — and 2026 is the year the calendar loads up.

Here's the regulatory arbitrage that isn't getting enough attention: they're not betting on aging itself. They're betting on clearly recognized diseases like Alzheimer's tau pathology, Alexander disease, and Angelman syndrome — conditions with established FDA pathways. That's a cleaner regulatory path than anyone chasing "longevity" directly.

| Catalyst | Timeline | Risk Profile |

|---|---|---|

| Zilganersen NDA + launch | 2026 | FDA-friendly disease target + rare neurology |

| ION582 Phase 3 data | 2026 | High unmet need + Angelman syndrome |

| BIIB080 Alzheimer's data | 2026 | Mechanism validation + Tau pathology |

IONS has its share of speculative bets, but a higher beta than large caps and catalysts grouped into one calendar year. $12.50 per $100 allocation. Now, for those of you who want to really bet on biology, you have to be prepared to stomach lottery tickets.

Small-Cap Pick #5 — Unity Biotechnology (UBX): The Senolytic Lottery Ticket

Full disclosure: Unity Biotechnology trades at a market cap of ~$3.4M as of May 2026 — we're talking penny stock, micro-cap territory, not some respectable biotech play.

You want to know why this slot exists at all? Because UBX is the only US-listed clinical-stage pure-play senolytic company on the market. The only one. No other public vehicle exists for this concept — senolytics that hunt down senescent cells, the zombie cells your body forgot to kill — and clear them out before they drive aging-related decline.

What you're actually buying:

- Peter Thiel and Jeff Bezos backing the play. Thiel didn't wire money into UBX because it sounded cool. Bezos didn't either. That's all the conviction signal you need.

- An ophthalmology program as the near-term FDA-approvable shot — disease target, not aging itself, so the regulatory path is cleaner.

- The only liquid public vehicle for the senolytic thesis — until Retro Biosciences or Altos Labs goes public.

This is binary. Illiquid. Violently volatile. If UBX hits clinical validation, the repricing from this floor will be staggering. If they don't, you're holding a lottery ticket that didn't print.

This is sized accordingly at the speculative edge of your $12.50 small-cap allocation — not a portfolio position, a lottery ticket with hard risk tolerance requirements. For investors who'd rather own the concept than wait for the ETF.

Ranked Recommendations: The BIO-OPTIMIZED Top 5

Moderna owns the platform layer. Cancer first, aging next. The mRNA doesn't care what disease it targets — that's the bet.

Eli Lilly is already cashing checks inside longevity. Mounjaro prints. Donanemab Alzheimer's revenue hits 2026–2027. You're not betting the science works — it already is.

AbbVie is the anti-aging market. Botox. Juvéderm. Injectables at 83%+ margins. Not pipeline fantasy. Recurring revenue that biology can't escape.

Ionis splits the difference. Active 2026 catalysts. Zilganersen launch, Phase 3 readouts. RNA therapy hitting disease, not "aging" — cleaner regulatory path. Don't sleep on that.

Unity is the swing. Micro-cap. Binary outcomes. Only pure-play senolytic vehicle on the public market. Billionaire backing (Thiel, Bezos) signals the science isn't vaporware. Clinical validation reprices from zero.

Three anchors. Two swings. One thesis.

The Closing Argument: Bet on the Biology

Here's the question I keep asking myself: where's the money actually going right now?

Capital's flowing upstream into life extension biotech before the mainstream arrives. Not because aging's been solved. Because billionaires already have access — and they're betting like it.

LOOKMAXXING and BIO-OPTIMIZED seem like distant cousins but what they really are is storefronts and the factory floor. Lookmaxxing is how consumers see it — their kids getting fillers, GLP-1 normalizing injectables, aesthetics going clinical. Bio-Optimized is where the actual science happens and where the capital is quietly accumulating.

The Numbers, The Fog, and Why It Matters

Anti-aging market CAGR ranges from 6.7% to 21.5% — depending on scope. One thing's clear: up. The range isn't weakness — it's fog. And fog means early access.

Let's not kid ourselves. There's definitely a regulatory risk with the FDA. Aging isn't a disease, and there's no definitive approval pathway. That doesn't one-shot the theme altogether. But it means every catalyst in this report is an indirect play on longevity, not a direct one. Price that fog into every position size.

The Thing Nobody Admits

Rich people always get to the party first. Not cynically — just observing the pattern. All the bleeding-edge stuff (epigenetic reversal, cellular rejuvenation, personalized cancer vaccines) started in private labs funded by billionaires, then moved into clinical trials, then into the public markets. That's the arc. We're somewhere between private lab and clinical trial on most of this. Which means the public market is still early.

Whether you're throwing lottery ticket money at a senolytic script or you've got a billion, you're trading the same thing. You can get the biggest eventual returns by betting early on things that look completely deranged before they look obvious.

This still looks deranged.

Good. That's when you buy.

KALYUG CAPITAL — BIO-OPTIMIZED — 2026