House Thesis: Why Chance Matrix Is The Trade

If we play the game everyone’s playing, who’s actually winning?

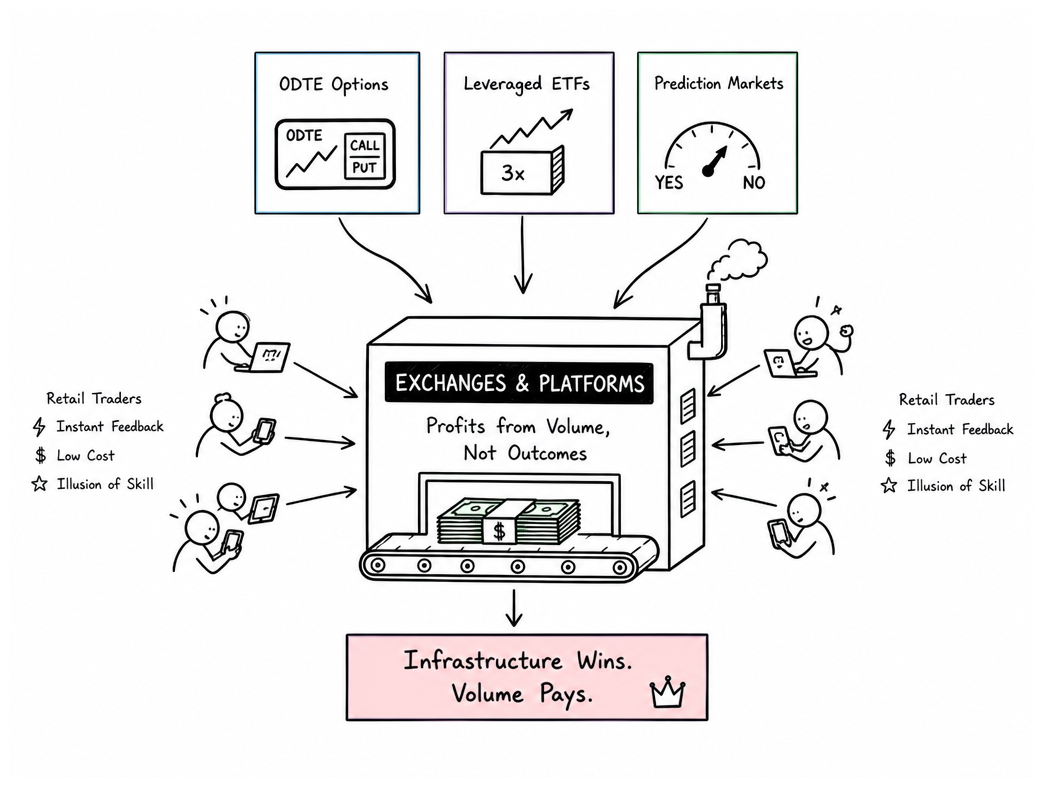

It’s not the retail trader who puts rent money on 0DTE SPX puts. Not the degen who goes all-in on prediction markets. Not the sports bettor riding a same-game parlay. What kills you: this infrastructure feels like freedom. Zero commissions. Instant feedback. Dopamine on a six-hour drip. But it was engineered to feel that way — because the people who built it get paid whether you win or lose.

| Signal | Volume Reality |

|---|---|

| 0DTE Options | Half of S&P 500 daily volume expiring same day |

| Leveraged ETFs | Daily reset bleeds value sideways — platform pockets the spread |

| Prediction Markets | $64B annual volume, raked in by platforms, not bettors |

The real alpha? It’s in owning infrastructure, not speculation. Exchanges don’t forecast markets. They monetize the fog. Your every trade is their toll. Your every loss is their revenue. Your every win is their marketing budget.

“Just because you understand the architecture doesn’t mean you stop playing. It means you stop pretending you’re playing a different game.”

So here’s the Chance Matrix thesis: everyone is either in the business of owning the dealers, or feeding the dealers. Five stocks that own the table across every format speculation takes — derivatives, prediction markets, sports betting. Own the toll road. Let everyone else race on it.

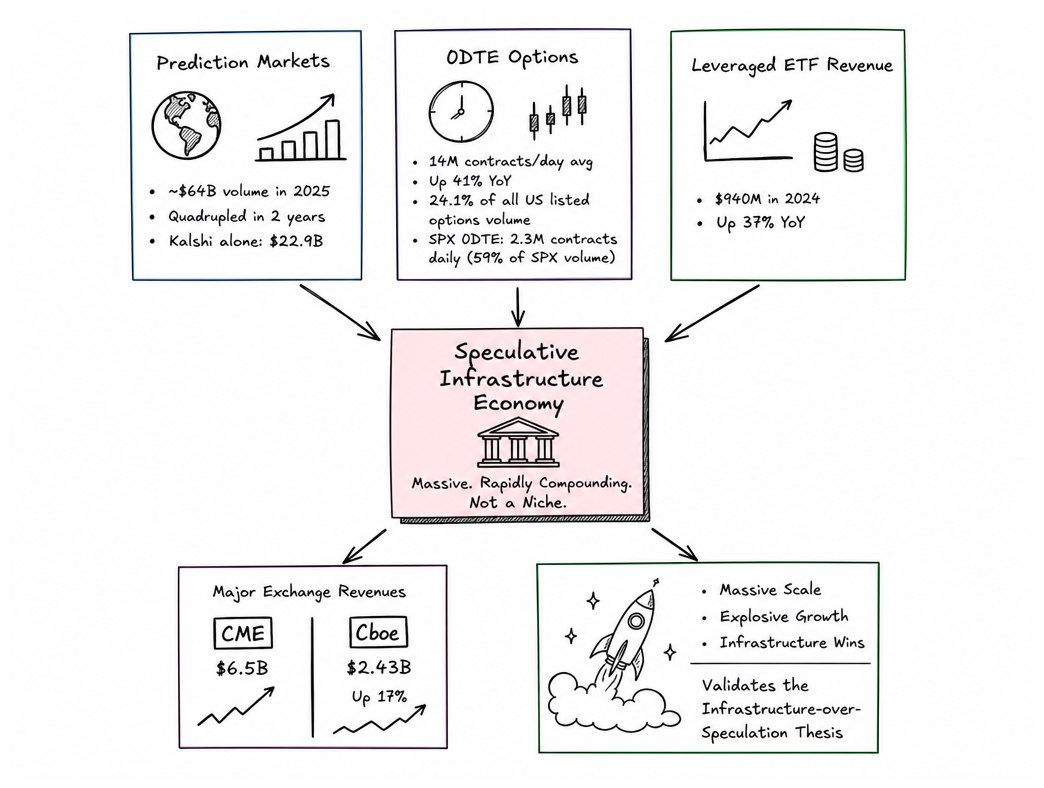

Market Sizing: What Is The Size Of The Chance Matrix Economy?

Infrastructure never cared which side of a deal wins or loses. It’s built to be agnostic. All it cares about is volume. And the volume numbers here are not small.

In 2025, 0DTE options — contracts expiring the same day they’re traded — hit 14 million contracts per day, up 41% YoY. SPX 0DTE options alone account for 59% of all S&P 500 daily volume. That’s not a trend. That’s the new floor.

| What’s Moving | Volume / Revenue | Signal |

|---|---|---|

| Prediction Markets (Global) | ~$64B annual volume | Quadrupled in 2 years |

| 0DTE Options (Daily Avg) | 14M contracts | +41% YoY |

| SPX 0DTE’s Share | 59% of SPX daily volume | Now the structural floor |

| Leveraged ETF Revenue (6 providers) | $940M in 2024 | +37% YoY |

CME Group hauled in $6.5B in 2025. Cboe saw $2.43B in net revenue — 17% growth — driven entirely by short-dated offerings. Six leveraged ETF providers pulled $940M in fees. Every retail wave discovering leverage feeds the beast. Every platform reducing friction expands the addressable market. Every new state legalizing sports betting is a new revenue stream with zero marginal cost to the infrastructure layer.

Thematic Narrative: One Pattern, Four Markets

0DTE options, leveraged ETFs, prediction markets post-2024, sports betting — they look like four trends. They’re one appetite. Same hunger, different interface.

- Instant feedback loops — immediate dopamine rush, answers in hours

- Zero-commission entry — that’s how you know it’s the hustle

- The illusion of skill — you’re making a call. You’re feeding the table.

- Infinite replay — daily expirations, daily resets, daily matchups

Cboe launched daily options expirations in 2022 and called it “normal.” Leveraged ETFs passed $1T in AUM. Prediction markets went from novelty to mainstream. Sports betting crossed 25 states. Each format is the same extraction architecture wearing a different costume. And the companies that own the pipes, the venues, the clearing rails — they print in all conditions.

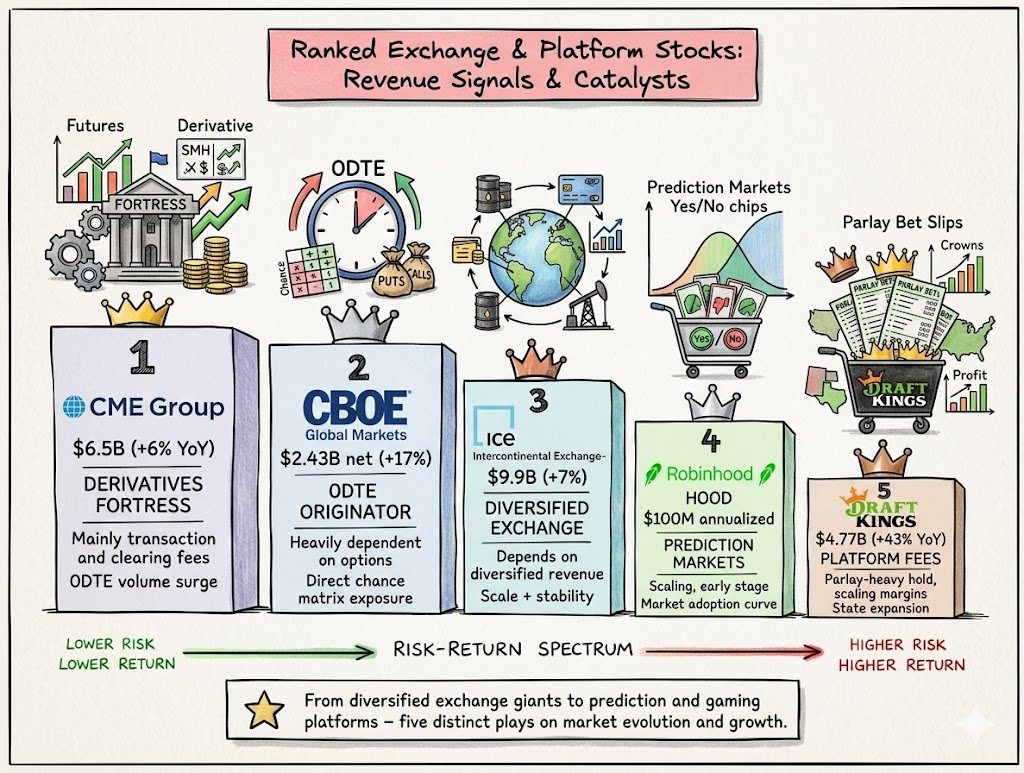

Large-Cap Picks — The Fortresses

The Derivatives Fortress

Simple question: where does every dollar in derivatives have to flow through? CME Group. Not just because they’re the fastest or the biggest — because they’re the only regulated venue that clears the instruments the entire institutional machine depends on. They’re not competing for volume. They are the volume.

In 2025, CME averaged 28.1 million contracts per day (+6%), with clearing and transaction fees as the core revenue engine. Market data revenue grew 13% to $803M. Whether it’s a bull market, bear market, or sideways hell — market data charges every single day regardless of which way prices move.

No one’s touching their moat. Europe and China have their own markets, but CME is the market for USD-denominated derivatives. The short-dated explosion runs through their pipes. Daily average volume for E-mini S&P 500 options grew from ~100,000 contracts to over 1.7 million. Because the model is primarily fixed costs, every incremental contract is near-pure margin.

Position: Core Large-Cap. They profit in screaming volatility and dead calm markets alike. The ultimate all-weather infrastructure asset.

The 0DTE House

Imagine the owner of a casino consistently earning more than all those playing at its tables. That’s Cboe. With their 2022 launch of daily options expirations — now expanded to five days a week — they didn’t just create a product. They engineered an addiction cycle that now accounts for the majority of their revenue.

The real story of 2025: net revenues of $2.43 billion, up 17%. Total revenue of $4.71B. Their share of U.S. options market volume has held and grown as they commoditized the short-dated format. Revenue doesn’t care whether you win or lose — it flows from volume, full stop. Bull market, bear market, sideways? Doesn’t matter. More chaos means more hedging, more speculation, more daily expirations.

Volatility? Irrelevant to them. More volatility means more hedging. Less volatility means retail still can’t help itself and keeps playing. The revenue engine is symmetric. They built the table. They collect the vigorish. Every. Single. Hand.

Position: Core Large-Cap. The 0DTE thesis made flesh. Near 52-week highs and still accelerating.

The Quiet Giant

Everyone’s watching Cboe’s 0DTE fireworks. But does the flashiest trade always win? ICE is the machine that’s been quietly compounding for two decades while everyone stares at the noise. They moved 2.4 billion futures and options contracts in 2025, pulled in $9.9B in consolidated revenues, and run some of the most critical market infrastructure on earth — including the NYSE.

Here’s where it gets interesting: Cboe lives or dies on 0DTE. If tomorrow regulators decided daily expirations were too spicy, their entire thesis wobbles. ICE? They run energy markets, credit markets, mortgage data (ICE Mortgage Technology), fixed income clearing. Diversification isn’t just risk management — it’s antifragility. Q1 2026 net revenue rose 20% to $3B, adjusted EPS up 37% to $2.35.

Currently in a W4 consolidation, pulling back from the $189 52-week high. That’s the entry. While showmen burn out, ICE compounds scale quietly. No dopamine hits. Just relentless, boring infrastructure printing in every market condition.

Position: Large-Cap Compounder. Cboe is the carnival barker. ICE owns the whole building.

Small-Cap Picks — The Casino Floor

Now we leave the fortress and venture into the casino floor. But here’s the thing — who actually makes money when retail goes feral? Not retail. The platform.

The Prediction Market Dark Horse

Prediction markets are seeing massive volume from multiple platforms. But there’s only one winning condition in this game: owning the rails the bets run on. Robinhood reported $100M in annualized prediction market revenues. While small relative to their options business, it’s already profitable. The mechanism? A 2% fee on winning bets — but the real play is that this routes users into the Robinhood ecosystem where they also trade 0DTE options and leveraged ETFs.

One thing missing from the pricing thus far: HOOD’s retail base is already the most active options trading cohort in the market. Adding prediction markets is not a separate business — it’s upselling the same customer. If volumes scale 5x from here, the revenue impact is sudden and dramatic, and no one is modeling that yet.

Currently recovering from the $62 lows, forming what looks like a W1 new impulse. High beta, but the platform flywheel is intact: more products, same sticky customer base, expanding margin profile.

Position: Small-Cap High Beta. Asymmetric if prediction markets scale. Size appropriately.

The Sports Betting House

Here’s what nobody wants to admit about sports betting: DraftKings isn’t the degenerate gambler. It’s the bookie. And the bookie always wins. Every parlay placed, every same-game multi, every futures bet — DraftKings takes a structural margin on every single one regardless of the outcome. The house edge is baked in. Scale is the only variable.

The 2024 numbers told the story: $4.77B in revenue, up 43% YoY. Monthly unique payers keep compounding as state by state legalization rolls through the political system. Same-game parlays are the 0DTE options of sports betting — massive positive expected value for the platform, massive negative expected value for the bettor, and structurally addictive to the customer.

The regulatory moat is real. Twenty-five-plus state licenses aren’t just expensive to obtain — they’re expensive to replicate. Customer acquisition cost is compressing as markets mature. The cash burn phase is ending. The existential risk is federal overreach or state reversal — possible, but the political current is running toward more legalization, not less.

Position: Small-Cap High Beta. DKNG is the Chance Matrix thesis wearing a jersey instead of a suit. Same extraction architecture, same infrastructure advantage, different aesthetic.

Verdict: The Five Ranked

The exchanges are the house. They don’t need to pick winners. Whether you’re printing or burning cash on every single contract — they collect. CME and CBOE are the highest-conviction positions: toll roads on the derivatives explosion with near-zero downside to volume. ICE is the antifragile compounder — W4 pullback is the entry, not a warning.

HOOD plays a different game. High beta, a little unhinged — but that’s the point. Prediction market revenue is invisible in the model right now. If it scales 5x, the stock re-rates dramatically. Size it as a high-beta asymmetric position, not a core hold.

DKNG is the Chance Matrix in a stadium. Every parlay is a 0DTE option with a jersey on it. Same dopamine architecture. Same extraction math. The cash burn phase is ending. Once this business reaches operating leverage, the margin profile flips hard. The question is patience.

Will you decide to catch the value or feed it?

Own The Table. Collect Every Hand. — Kalyug Capital 2026