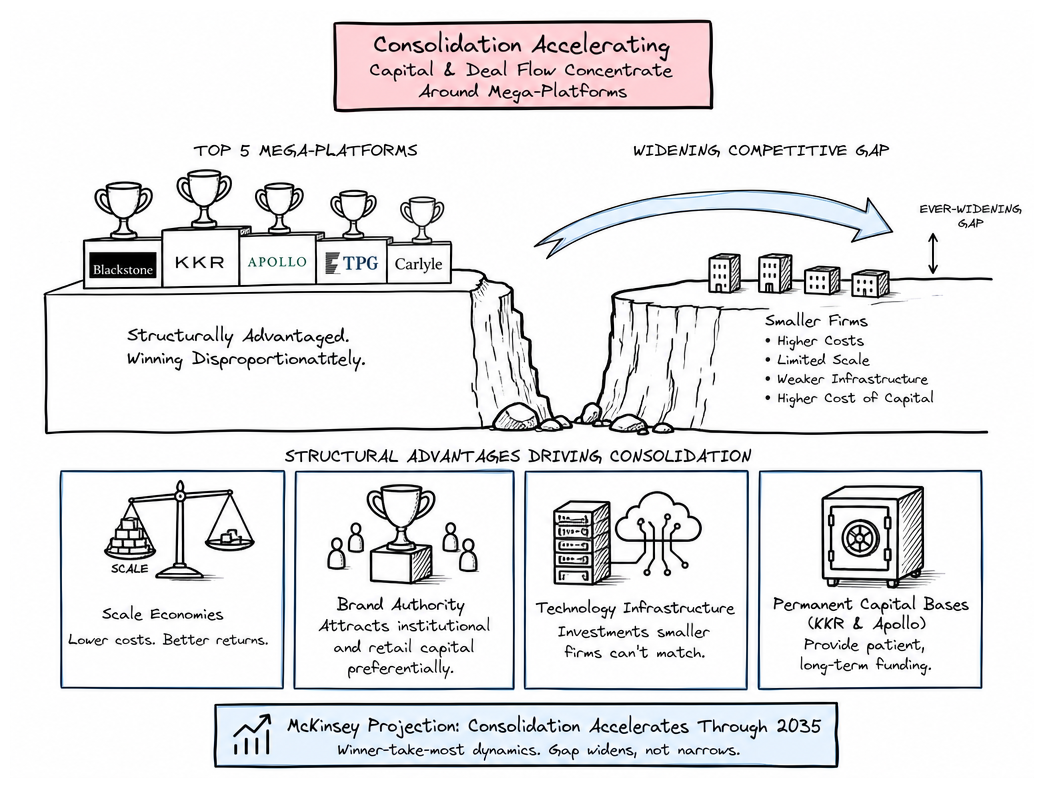

Capital is flooding out of public markets. The firms absorbing it aren't passive recipients — they're actively engineering the architecture of where institutional wealth goes next. McKinsey estimates that competitive structure consolidates by 2035, with fewer than 20 firms controlling the majority of alternative asset flows. Five of them are already pulling away.

| Company | Ticker | Primary Lane |

|---|---|---|

| Blackstone | BX | Alternatives colossus |

| KKR & Co. | KKR | Multi-asset execution |

| Apollo Global Management | APO | Credit-first platform |

| Ares Management | ARES | Direct lending leader |

| Hamilton Lane | HLNE | Institutional gateway |

There's no doubt about consolidation. The question is: are you on the right side of it?

Ranking Methodology

Sorting by AUM misses the point. There's little upside in owning the biggest firm if it's also the most exposed. Four criteria drove the ranking:

- Vision — A view on where capital flows will be in a decade, not the next quarter

- Market Position — Proprietary deal flow, sticky clients, established institutional relationships that competitors can't replicate quickly

- Execution — Capital raises that actually hit. Fund vintages that performed. Forecasts that held

- Financial Health — Solid fee-related earnings, margin strength, balance sheets that can weather a PE cycle downturn

| Category | Market Cap Range | Examples |

|---|---|---|

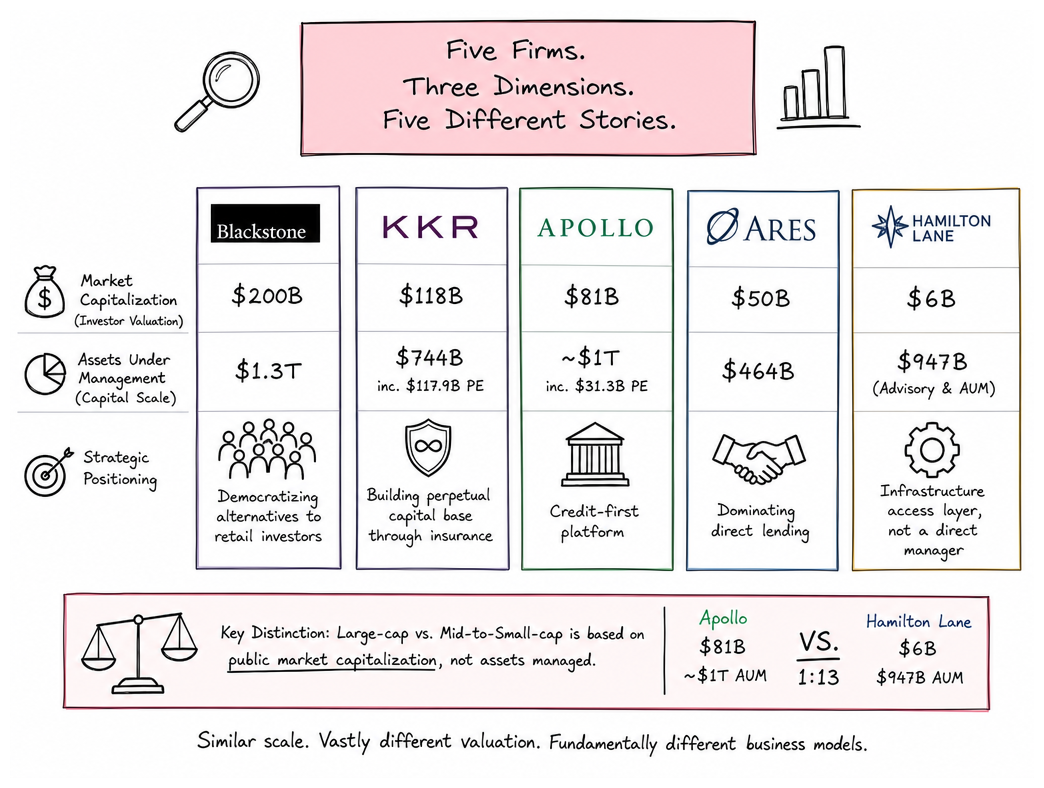

| Large-cap | $80B+ | BX, KKR, APO |

| Mid-to-small-cap | $6B–$50B | ARES, HLNE |

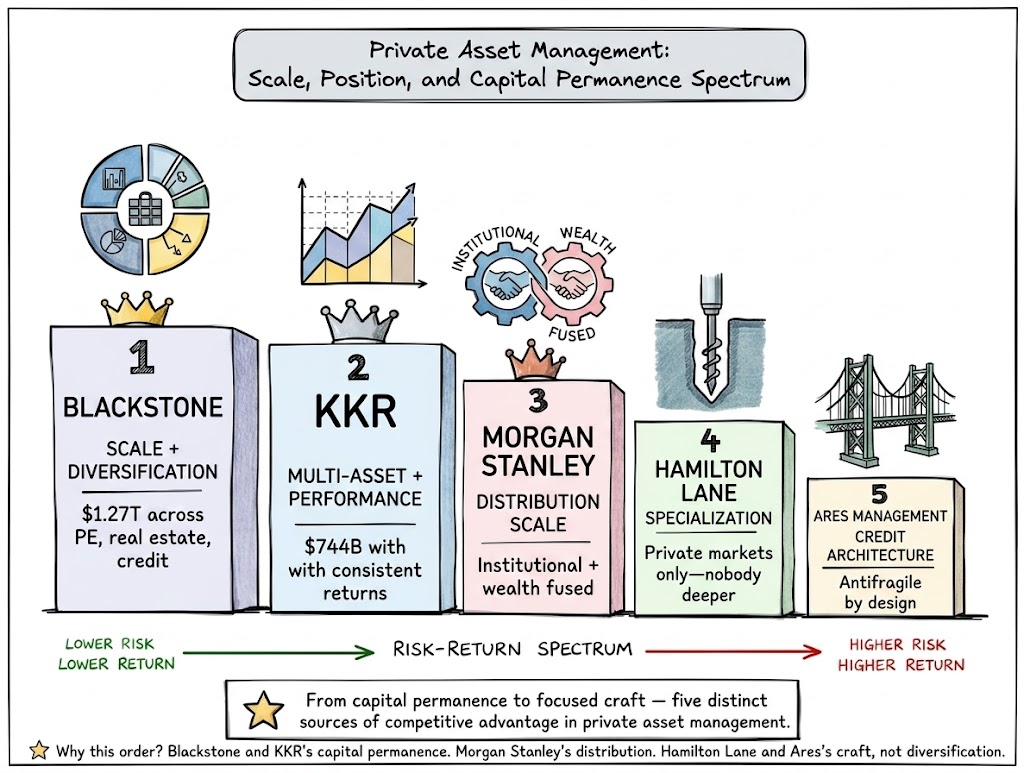

#1 Blackstone (BX) — The Alternative Asset Colossus

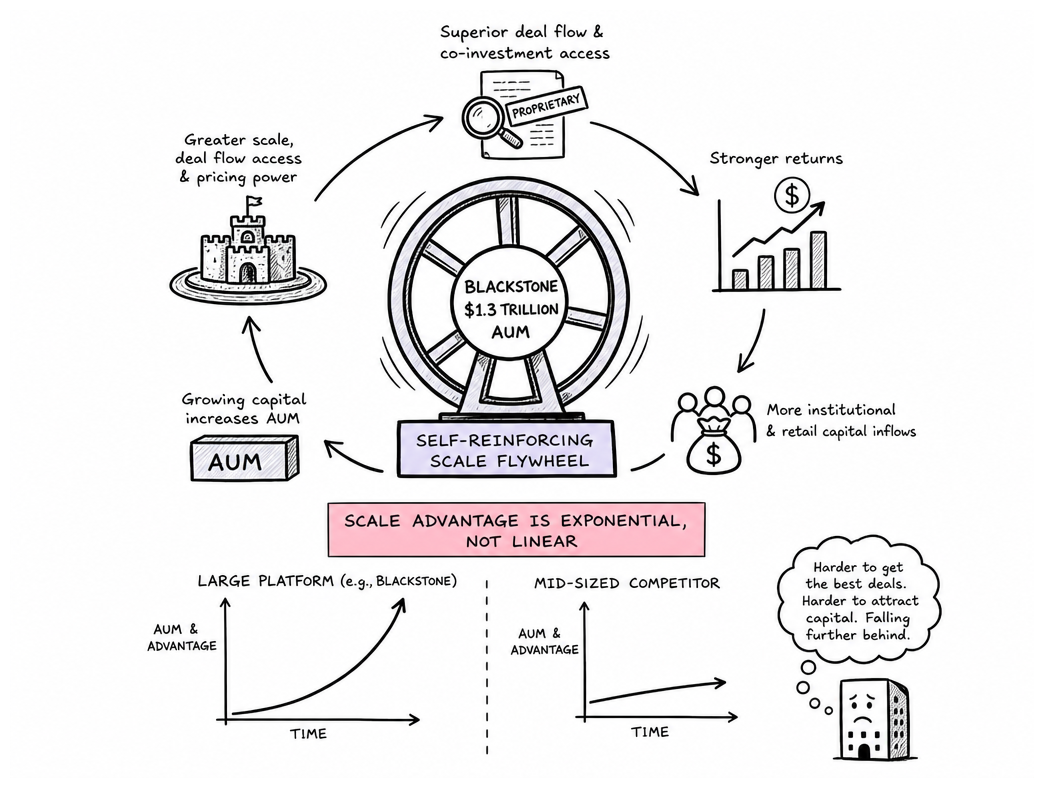

Blackstone is a story of structural size that compounds on itself. Market cap hovers around $200B. The group manages $1.3T in AUM with $1.1T in private markets. But scale alone isn't the story.

The story Blackstone figured out — which everyone else kept chasing — was that alternative assets don't need to stay institutional. BREIT opened the retail floodgate. Now every competitor is building a retail alternatives product. Blackstone built the distribution first.

| Metric | Value |

|---|---|

| Market Capitalization | ~$200B |

| Total AUM | $1.3T |

| Private Markets AUM | $1.1T |

- Brand dominance — When a billion-dollar pension fund asks "where does serious capital go," Blackstone lands first. That's not marketing. That's decades of compounded trust

- Proprietary deal flow — Bigger funds attract better deals. Better deals attract more capital. It's recursive. It's a flywheel with no obvious off-switch

- Diversification across PE, real estate, and credit — One vertical tanks, three others still print

Financial health holds. Fee-related earnings keep printing. Distributable EPS stable. Blackstone co-invests alongside LPs, aligning incentives in a way that pure fee shops can't credibly replicate.

#2 KKR — The Multi-Asset Execution Machine

Blackstone chases fundraising cycles. KKR is building a capital base that doesn't need one. $118B market cap, $744B total AUM including $117.9B in private equity. But the key differentiator is structural — not size.

- Global Atlantic acquisition — permanent, patient insurance capital that funds deals without LP redemption pressure. The GP incentives are structurally aligned

- $618B in private markets AUM growing in credit and infrastructure — the compounding revenue streams that don't flash in bull markets but don't collapse in bear ones either

- Balance sheet co-investment — skin in the game means GP incentives are locked into long-duration outcomes, not quarterly optics

The real inflection here is the insurance capital engine. Unlike Blackstone, KKR doesn't rely on fundraising cycles to fund deployment. The capital is permanent. The compounding is structural. While Blackstone's brand dominance and retail distribution advantage are wider right now, the structural capital advantage KKR is building makes this a 2030 question. By then, the gap narrows.

#3 Apollo Global Management (APO) — Credit-First, Everything Else Second

This is a different animal. Blackstone and KKR are capital vacuum cleaners and asset-class empire builders simultaneously. Apollo made a different bet: own the credit stack so completely that deal cycle exposure becomes almost irrelevant.

A credit machine that doesn't care about deal cycles.

Athene is the load-bearing wall — insurance capital guaranteeing low-cost, permanent funding. KKR replicated this with Global Atlantic. Apollo built it first and has been running it longer.

| Factor | Apollo's Edge | The Trade-Off |

|---|---|---|

| Capital Source | Athene insurance — guaranteed low-cost permanent capital | Smaller PE base limits carry upside in bull markets |

| Income Stability | Credit fees + annuities = cycle-resistant | Boring in bull markets |

| Institutional Positioning | Direct lending relationships built over decades | Compounding from smaller AUM base |

Apollo isn't flashy, but it's the alternative asset play for investors who don't want to gamble on the PE cycle. When the cycle turns, Apollo's defensive posture becomes the offensive play.

#4 Ares Management (ARES) — Mid-Cap Direct Lending Leader

When Apollo gets fatigued with credit-first management at mega-cap scale, here's what's leaner, hungrier, and more agile. Ares runs $464B in AUM with a market cap around $50B. Not a super giant — but the moat is older than most people's careers in finance.

- Direct origination relationships — Middle-market borrowers know Ares. They don't shop the loan around. Speed and certainty of close is the product

- BDC platform expansion — Business Development Company vehicles lock in recurring management fees from long-dated credit books

- Real estate credit foray — Expanding horizontally. Not betting everything on one asset class

Proportional AUM growth from a smaller base means compounding at scale hasn't really started yet. Ares has room that Blackstone doesn't. For investors seeking alternative asset exposure with real insulation from PE deal cycle swings, this is the play — but the PE cycle risk is real. Don't ignore it.

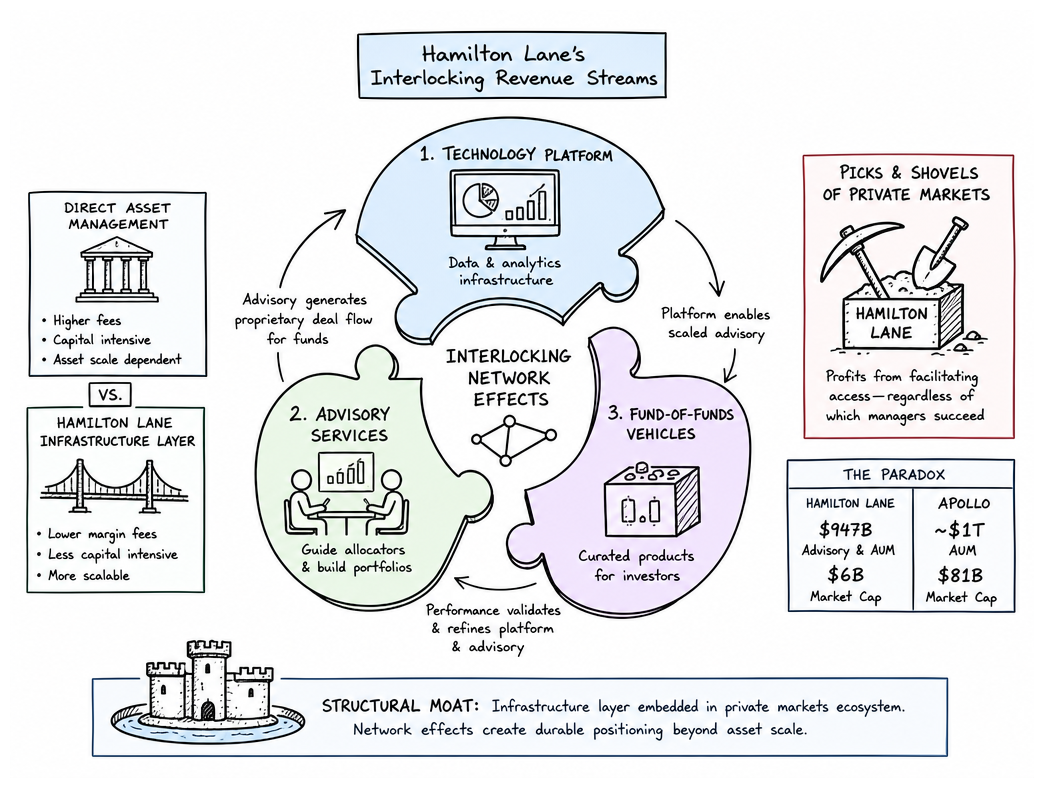

#5 Hamilton Lane (HLNE) — The Institutional Access Gateway

Scale matters. But position is everything. With a $6B market cap and $947B in AUM, Hamilton Lane isn't deploying that capital — it's the rails the capital runs on. KKR executes the deals. Apollo finances them. Ares lends into them. Hamilton Lane tells the institutions which ones to touch and builds the platform that makes it possible.

| Revenue Stream | Function | Cyclicality |

|---|---|---|

| Technology Platform | Data aggregation, allocations management | Low — runs regardless of deal flow |

| Advisory Services | Connecting institutions to private markets | Medium — tied to fundraising momentum |

| Fund-of-Funds | Portfolio-level PE/credit exposure | Medium — carries some deal risk |

This bundling is the moat. Most alternatives shops pick a lane and own it. Hamilton Lane fused three. Advisors recommend them. Institutions trust them. Retail access is expanding systematically — lowering barriers and capturing the next wave of capital flowing into private markets.

The catch: when private markets fundraising slows, HLNE feels it fast. Unlike Blackstone's diversified cushion, Hamilton Lane's revenue is more directly correlated to deal and fundraising momentum. This is the infrastructure play — the firm that profits from the system, not the players.

How These Five Are Changing Institutional Wealth

Capital is flooding out of public markets. These five are not only capturing the flows — they're building the infrastructure that makes the shift permanent. Three structural forces are reshaping the wealth layer simultaneously:

| Force | What's Happening | Why It Matters |

|---|---|---|

| Direct Indexing | Personalized mandates, tax loss harvesting, custom benchmarks now baseline | Institutions demanding bespoke — our five are the architects |

| AI Adoption | Morgan Stanley advisers at 98% adoption — wholesale transformation | Speed signals inevitability. The firms with data infrastructure win |

| Data Infrastructure | JPMorgan Fusion aggregating private-markets data into standardized feeds | Our five rank among the biggest beneficiaries of standardized access |

"By 2035, competitive structure consolidates into fewer than 20 firms controlling the majority of alternative capital flows." — McKinsey

Translation: acceleration in consolidation. All five firms — Hamilton Lane among them for its picks-and-shovels positioning — are structurally placed to compound from the shift rather than fight against it.

Frequently Asked Questions

| Firm | Total AUM | Private Markets Focus |

|---|---|---|

| Blackstone | $1.3T | PE, real estate, credit |

| KKR | $744B | PE, real estate, infrastructure |

| Apollo Global Management | ~$1T | Credit, PE, real estate |

| Ares Management | $464B | Credit, PE, real estate |

Final Verdict: Who Wins the Decade

The ranking rests on four load-bearing walls: vision, moat, execution proof, financial fortress. Blackstone and KKR own the top two slots on those criteria today. The structural capital advantage KKR is building with Global Atlantic makes 2030 a different conversation. Apollo's credit defensiveness makes it the all-weather play. Ares and Hamilton Lane are the growth-oriented expressions of the same secular theme from a smaller base.

| Best Fit | Risk Appetite | Why |

|---|---|---|

| $BX, $KKR | Conservative, long-horizon | Proven execution, fortress balance sheets, infrastructure asset diversity |

| $APO | Balanced defensive | Less cyclicality, credit moat, Athene permanent capital engine |

| $ARES, $HLNE | Growth-oriented | Compounding from smaller base, moderate cyclicality, higher beta to deal flow |

The next decade will be shaped by the firms that own private markets infrastructure. The question isn't if the shift happens — it's already here. The question is whether your portfolio is on the side that collects the rent, or the side that pays it.