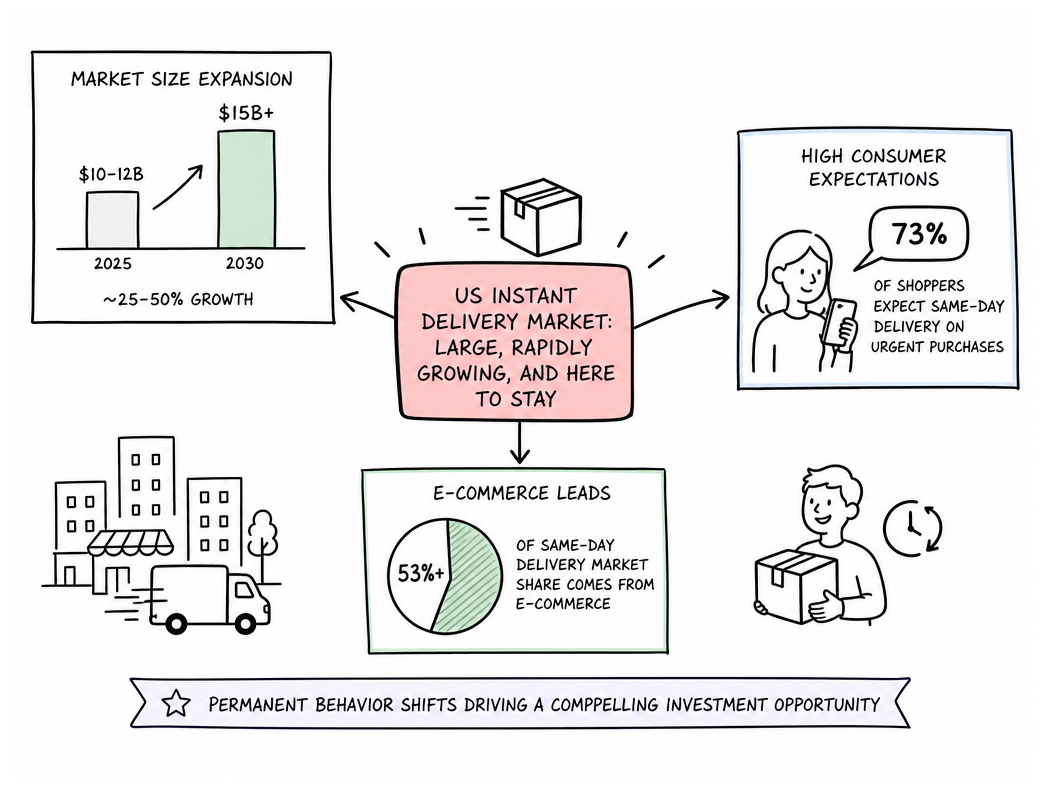

The obsession with speed is definitely real. It's now expected for US shoppers to get same-day delivery on urgent purchases. What was once a luxury differentiator is now the floor of expectation. What you're actually seeing:

| Company | Ticker | Play |

|---|---|---|

| DoorDash | DASH | Last Mile Logistics at Scale |

| Uber Technologies | UBER | Global Delivery Platform Ambitions |

| Amazon | AMZN | Prime-Driven Infrastructure Moat |

| Instacart | CART | Grocery-Tech Platform |

| Grab Holdings | GRAB | Southeast Asia Super-App Giant |

Will quick commerce stocks win? More importantly — who will own the last mile's complicated endgame, and will the market price it correctly before the window closes?

Why These Five Companies

Your why behind a rank is often as important as the what of the ranking itself. When putting this list together, four criteria drove the selection:

- Strategic Vision — What are these companies' actual roadmaps? An unstoppable force for dominance, or just leasing the last mile?

- Competitive Moat — Last-mile delivery capability weighted heavily. It's the chokepoint. Proximity to customer, delivery density, automation investment.

- Execution Track Record — How fast are they moving? Market share trajectory versus stated vision.

- Financial Health — Profitability, unit economics, cash burn. A beautiful vision that eats cash and never pays rent is still a bad trade.

Notably absent: GoPuff — a private company that's considered a leader in the US quick commerce market. Not publicly listed, so not on this list. The ranking is purely about where public-market capital can flow.

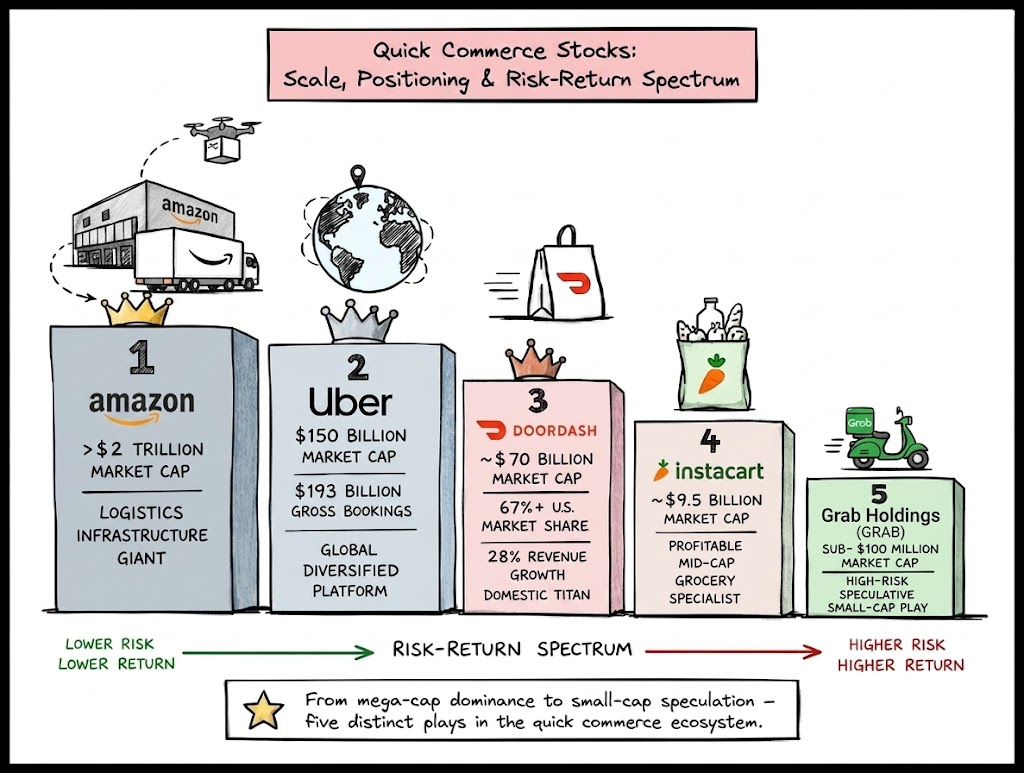

#1 DoorDash (DASH) — The Undisputed Domestic Titan

When it comes to leadership in the domestic quick commerce market, DoorDash is leading the pack. The food delivery giant doesn't just dominate the category — it's actively building the infrastructure to own it permanently.

Here's what most people miss: while DoorDash is an app, it's not just building an app. The company aims to build the "operating system of local commerce." DashMart — the convenience network — proves this isn't a tagline.

"We're building an autonomous delivery platform, because ultimately we think different modalities will compete with in-store retail itself."

DoorDash reported $13.7B in revenue for 2025. The execution metrics are equally telling:

- Two-wheel fleet growing 4x faster than car-based deliveries

- Bike drivers earn 10%+ more per hour than car drivers

- Cheaper, faster, better for drivers — the unit economics improve as the fleet evolves

On autonomous delivery: DoorDash debuted Dot, its autonomous robot, in September 2025 — a total commitment, not tinkering. Why #1? All three firing at once: dominance, autonomy, and scale. No competitor has all three simultaneously.

#2 Uber (UBER) — The Global Platform With Last-Mile Ambition

DoorDash is the food delivery leader in the US. But crowns are local and heavy things. Uber has a global business that happens to include delivery. The earnings call said it plainly: "$193 billion in Gross Bookings... a clear path to becoming the largest facilitator of local commerce on Earth."

Uber Eats is going head to head with DoorDash — same cities, same delivery merchants, same customers. The differentiation is the breadth of the Uber ecosystem: rides, freight, eats, all on a single platform driving cross-sell economics that DoorDash simply cannot match.

| Partner | City | Launch Date |

|---|---|---|

| Avride | Philadelphia | March 2026 |

| Coco Robotics | San Jose | April 2026 |

| Cartken, Serve Robotics & others | 10+ cities | Oct 2025–Present |

By late 2025 there were hundreds of thousands of robot deliveries across more than 10 cities. Durable last-mile moat = deep AV investments + strong Uber Eats momentum + scale of Uber's global platform.

The risk: when speed and iteration are critical, a focused approach outweighs financial diversification. DoorDash's full-stack commitment is the counter-argument. Which moat wins when the fog of uncertainty thickens depends on which scales faster — infrastructure or focus.

#3 Amazon (AMZN) — Logistics Infrastructure as Competitive Moat

Amazon reported $638B in net sales for 2025. While others are figuring out if unit economics matter, Amazon's been building fulfillment infrastructure for two decades. Prime. Fresh. Same-day. The moat is geological.

| Player | Delivery Speed | Market Position | Infrastructure |

|---|---|---|---|

| Amazon Fresh/Prime | Same-day (existing) | 53%+ e-commerce share | Unrivaled logistics |

| Walmart | 30-minute (select areas) | Direct large-cap rival | Retail-first approach |

| DoorDash | Fast (3rd-party) | Pure-play leader | Hyperlocal density |

Walmart's move into 30-minute delivery just proves Amazon's thesis — speed is the new standard. Why #3? Because instant delivery is not Amazon's narrative. It's not the story the market tells. Behind cloud, advertising, and AI, quick commerce hides in plain sight as a structural winner.

The risk cuts both ways: if quick commerce successfully commoditizes, Amazon wins by default — scale beats competition. If it fragments into hyperlocal niches, Amazon's infrastructure advantage may not translate as cleanly.

#4 Instacart / Maplebear (CART) — The Grocery Tech Platform Punching Above Its Weight

Amazon is the infrastructure's forward competition. DoorDash is the agility-driven pure play. But Instacart is something else: a profitable tech platform hiding inside a grocery delivery skin.

| Metric | 2025 Full-Year | Q1 2026 |

|---|---|---|

| Total Revenue | $3.74B (+11% YoY) | $1B for the quarter |

| GTV | — | $10B+ (13% YoY growth) |

| Adjusted EBITDA Growth | — | 23% |

| Market Cap | $9.5–9.6B | — |

"We're a leading grocery technology platform powering retailers." — CEO Chris Rogers

Underneath the surface of a consumer marketplace, Instacart is an operational backbone for 1,400+ retail partners. That's a switching-cost moat that platform investors consistently undervalue.

Why not higher than #4? Actual profitable growth and good unit economics, but still underpriced as an enterprise-facing platform. The risk: commoditization of grocery delivery erodes the retailer relationship moat over time.

#5 Grab Holdings (GRAB) — The Southeast Asia Super-App With Quick Commerce Dominance

Instacart's moat is retailer relationships. Grab doesn't need one — it is the infrastructure. With a market cap around $14.9B, Grab is the dominant super-app across Southeast Asia: ride-hailing, food delivery, grocery, financial services, all on a single app.

| Metric | 2025 Full-Year | Q1 2026 |

|---|---|---|

| Total Revenue | $3.37B (+20% YoY) | $1.0B (+23% YoY) |

| Deliveries Revenue | $1.8B (+21% YoY) | $510M (+23% YoY) |

| Deliveries GMV | $14.2B (+21% YoY) | $3.9B (+25% YoY) |

| Net Profit | $200M (first full-year) | $120M |

| Adjusted EBITDA | $500M (+60% YoY) | $154M (+46% YoY) |

Why does a Southeast Asian super-app belong in a US quick commerce ranking? Because the playbook is identical — hyperlocal density, multi-modal delivery, cross-sell economics — and the proof of concept is already printing cash.

The risk: geographic concentration. Grab's moat is Southeast Asia — Indonesia, Malaysia, Singapore, Thailand, Vietnam, the Philippines. Structural winner in the region, but US-listed exposure to EM currency and regulatory risk requires a longer investment horizon.

Not a pure-play US story, but arguably the strongest business fundamentals on this list that nobody's talking about. The kind of stock you buy when everyone's focused on the wrong geography.

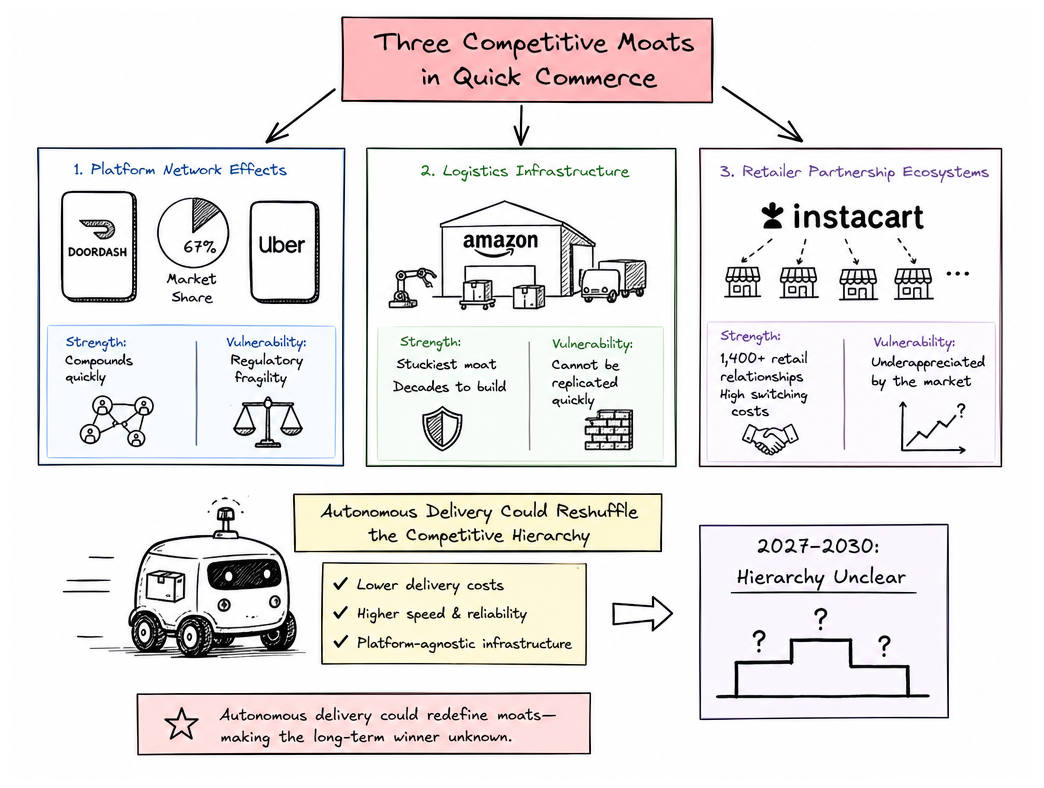

Which Moat Wins: Platform, Infrastructure, or Partnership?

Three distinct types of moats are locked in a slow-motion duel. Which one actually survives long enough to matter?

Platform moats (DoorDash, Uber) compound fastest — that's the seductive part. Until a regulator shows up and asks some uncomfortable questions about gig worker classification.

Infrastructure moats (Amazon) are stickier. It took Amazon decades to build its fulfillment network. It cannot be replicated quickly. The durability is real but the capital intensity is also real.

Partnership moats (Instacart) are habitually overlooked. Myriad retailer relationships, like 1,400+ relationships with major chains, create switching costs that are invisible until someone tries to move.

| Moat Type | Speed | Durability | Vulnerability |

|---|---|---|---|

| Platform (DASH/UBER) | Fastest compounding | Fragile under regulation | Policy risk |

| Infrastructure (AMZN) | Slowest to build | Most durable | Capital intensity |

| Partnership (CART) | Moderate scaling | High switching costs | Retailer concentration |

Autonomous delivery is one of those things that sounds futuristic until DoorDash deploys 10,000 robots and Uber has partnerships in 10 cities simultaneously. The timeline just got shorter.

No single winner. But fragmentation doesn't mean stasis — it means the next shock could come from any direction. Autonomous delivery, regulatory restructuring of gig classification, or a logistics bankruptcy consolidating the field overnight.

Volatility, Alpha, and the Chaos Beneath the Surface

Quick commerce stocks aren't dividend plays. They're high-beta growth names — violently repriced on a tariff tweet, a DOL ruling, a competitor partnership announcement. The alpha is in the entry point.

The sector is still nascent. Market chaos will create openings. The real question is whether you're positioned to take them when they appear — or whether you'll be reading about it after the move.

The Bottom Line: Five Stocks, One Secular Trend

Five stocks betting on one sector that hasn't yet figured out what it is, but that the market has already realized is worth trillions. The entry windows appear in the volatility. The conviction comes from the structural story underneath.

Unmatched 67%+ market share. 28% revenue growth. Autonomous delivery infrastructure actively deployed. The only pure-play with all three competitive pillars firing simultaneously.

$193B in Gross Bookings. Global reach. AV deployment momentum in 10+ cities. The risk is diversification diluting focus — the opportunity is that global optionality doesn't get priced in until it's obvious.

Logistics advantage absurdly hard to match. Prime flywheel doesn't break. Quick commerce is just another product line sitting on infrastructure that took 20 years to build.

Growing quickly. Profitable. Underfollowed. The market hasn't priced in that it's the top grocery tech platform — not a delivery app — powering 1,400+ retail relationships.

First full-year net profit. $3.37B in revenue growing 20% YoY. Deliveries GMV of $14.2B. The most profitable and fastest-growing company on this list that nobody in US finance is talking about.

Notable one to watch: ASAP/Waitr Holdings (ASAP) — Sub-$100M market cap, pure-play US delivery, M&A catalyst potential. High risk, asymmetric upside if the consolidation wave hits.