Why AI Infrastructure Stocks Are the Trade of the Decade

You've heard that the AI gold rush money isn't really going to the AI labs or the AI model makers. It's going to the picks and shovels. The unglamorous layer that makes the whole operation possible.

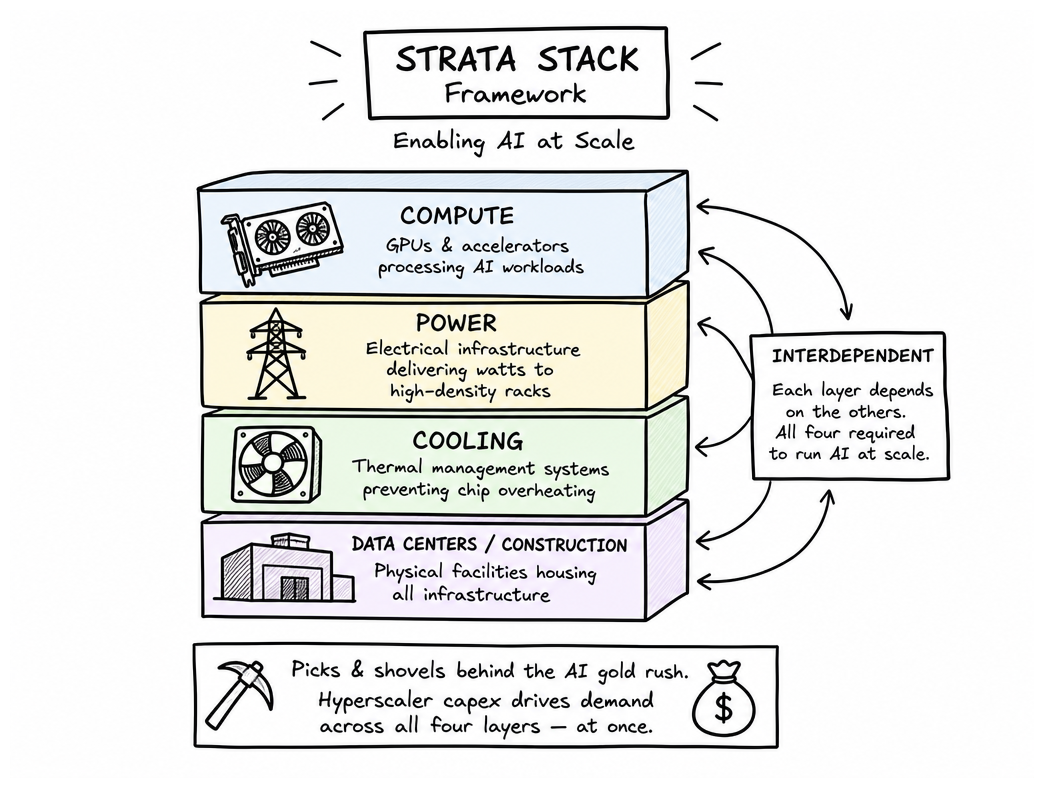

Hyperscalers are in a full sprint. They're running fast because they want compute power. But they also need data centers to house their compute, electricity to power it, cooling to ensure heat doesn't turn it to slag, and the networks that connect it all. That's the STRATA Stack. Four pillars. Data centers. Compute. Power. Cooling. (The whole damn thing collapses without any one of them.)

| Layer | What it Does | Why it Matters for AI |

|---|---|---|

| Compute | GPUs, TPUs, custom silicon | Runs the models, scales with demand |

| Power | Generation, transmission, distribution | AI data centers are power-hungry monsters |

| Cooling | Liquid cooling, thermal systems | Keeps hardware from frying at scale |

| Data Centers | Physical infrastructure and buildout | Where everything physically lives |

Here's the thing: this isn't general IT infrastructure. It's purpose-built. It's obsessive. Hyperscalers are dumping serious capital across all four layers. This demand is structural and it's here — and it's not slowing down.

Five of the best, ranked on four load-bearing walls: Vision — are they seeing where AI infrastructure is going? Competitive moat — what protects them from getting eaten? Execution track record — do they actually execute when it counts? Financial health — could they scale without imploding?

Three large-cap bedrocks. Two mid-to-small-cap risk bets that might give you sweaty palms. Now here are the kings.

#1 NVIDIA (NVDA) — The Undisputed Compute King

The gravitational center around which everything else orbits. At $4.58T market cap, this isn't just the largest company in the STRATA stack — it defines it.

The picks-and-shovels theory only works if one shovel manufacturer has locked down the entire mine. That's NVIDIA right now. Here's where most people get it wrong: they think NVIDIA wins because the hardware is fastest. Wrong. The real moat is CUDA — the software ecosystem that's been baking for two decades. Hyperscalers train their models on CUDA. Their engineers live in CUDA. Their codebases are written in CUDA.

Rip out an H100 and drop in an AMD MI300? Sure, technically possible. But you're now retraining everything. You're rewriting your stack. You're burning engineering cycles and chasing ghosts in unfamiliar code. That friction — that's the durable advantage. That's what keeps NVIDIA at 80–90% AI accelerator market share by revenue.

| Metric | FY2023 | FY2024 | FY2025 | FY2026 |

|---|---|---|---|---|

| Data Center Revenue | $15B | $47.5B | $115.2B | ~$194B |

| Total Revenue | — | — | — | $215.9B |

The execution is obscene. Gross margin around 71%, net margin 55.6% — these aren't sustainable forever, but they're sustainable long enough to reshape the entire infrastructure stack. And the Stargate Project? $500B of committed AI infrastructure capital. That's not optimism. That's a guarantee the compute demand runway extends further than anyone dared imagine.

- CUDA lock-in forces hyperscalers to absorb switching costs that make alternatives functionally invisible

- Competitive pressure from AMD and custom ASICs exists but doesn't threaten the core moat — just nibbles at the edges

- The software ecosystem is the load-bearing wall; hardware is replaceable, but the entire training and inference pipeline is not

#2 Broadcom (AVGO) — The Custom Silicon Challenger to Watch

Dominance breeds complacency. Broadcom spent three years quietly building a different kind of moat — not reliant on compute superiority, but on intimacy with the people actually building the infrastructure.

Broadcom's bet: custom silicon. No more paying a GPU price premium. Design exactly what Google and Meta want — XPUs, TPUs, custom ASICs for hyperscalers and their workloads — and make it so hard for customers to switch that they're hostage. Broadcom gets customers it simply can't lose, and hyperscalers get silicon they won't find elsewhere.

| Year | AI Revenue | Growth |

|---|---|---|

| FY2023 | $3.8B | — |

| FY2024 | $12.2B | +221% |

| FY2025 | $20B | +64% |

That's not trickling revenue. That's a flood. Broadcom now holds close to 10–12% of the AI accelerator market share, with analysts projecting 12–15% by 2026. Not enough to topple the king — but enough to matter.

Broadcom also owns AI networking: Tomahawk switches, Jericho routers, and the largely unseen plumbing that ties GPUs and custom silicon into larger AI systems. That's a second flywheel, and it's already spinning. As hyperscalers intentionally reduce NVIDIA dependence, Broadcom is sitting ready to take up the slack. The question isn't if custom silicon will take market share. It's how fast it'll happen.

#3 Vertiv Holdings (VRT) — Power and Cooling Infrastructure Backbone

No amount of custom silicon matters if your AI racks are turning to slag. Vertiv isn't glamorous. It won't trend on fintwit. But it's the infrastructure that makes the whole operation possible.

Vertiv manages power and thermal management from the grid to the chip: UPS, power distribution, liquid cooling, software orchestration. As Broadcom and NVIDIA slug it out over chips, Vertiv has the plumbing that prevents 1MW+ AI racks from transforming into expensive furnaces.

The Product Play: Liquid cooling takes heat away from dense AI clusters. UPS and power distribution convert voltage and provide backup power. And Vertiv OneCore — a pre-configured, factory-integrated infrastructure that trims deployment time by 50%, reduces space by 30%, and cuts total cost of ownership by 25%. Plug-and-play convergence configured for up to 600kW per rack.

So what's their moat? Integration. Power, cooling, software — all in one stack, sold by one vendor. As CEO Giordano Albertazzi explained, because they're operating on multiple layers, each unlocks efficiencies that enable the others, creating "compounding gains."

FY2025 revenue: $10.23B, up 28%. Backlog more than doubling to $15B — locking in 12–18 months of revenue before a single new deal is signed. Q1 2026: $2.65B, up 30%. FY2026 guidance: $13.5–14B with organic growth of 29–31%. In a world obsessed with vaporware, Vertiv has visibility most companies dream about.

#4 Quanta Services (PWR) — The Infrastructure Builder with a 25-Year Head Start

Someone needs to actually build it. 69,000 workers and 25 years of experience assembling massive, complex infrastructure. Not sexy. Not a tech company. One of the most defensible positions in the entire buildout.

The moat is embarrassingly simple — that's why nobody sees it. Quanta does 80%+ of its work in-house. That's 69,000 trained hands painstakingly built over 25 years. You can't copy that in a quarter's time. Or a decade's. The demand for data center construction is escalating, and labor scarcity gets deeper, not shallower. Every competitor chasing this TAM runs into the same wall: not enough craft workers. Quanta built the fortress before the siege began.

| Metric | Value | What It Means |

|---|---|---|

| Year-end 2025 backlog | $44B | ~12–18 months of forward revenue locked in |

| Low voltage electrical | 10–15% capture | Market leader in AI rack power distribution |

| Construction & facilities | 30–50% capture | Largest spend to come in physical buildout |

| TAM through 2030 | $885B → $2.4T | Business is ramping up |

Quanta is embedded in both sides of the power equation — data center construction and grid modernization, transmission line upgrades, utility infrastructure. AI compute demands electricity. The grid demands modernization to supply that electricity. Both currents flow through Quanta's business. A $44B construction backlog is nearly unprecedented.

#5 nVent Electric (NVT) — The Liquid Cooling Pure-Play Most Investors Are Missing

The bottleneck of an AI data center isn't chips. It's not power feed. It's cooling. nVent builds the thermal plumbing everyone needs but no one talks about.

A mid-cap at $28B market cap — which means it has room to move in ways the NVIDIA juggernauts simply don't. Eaton's priced for perfection. Vertiv's priced for perfection. NVT? Still flying under the radar as a thermal management play. The company is building liquid cooling enclosures designed from the ground up to handle what's actually happening in the data center right now.

- Q1 2026 revenue of $1.242B, up 53% year-over-year

- FY2026 guidance of +26–28% growth

- Revenue primarily driven by data center and liquid cooling

The midcap size adds to the upside. Large-caps have already priced in the AI boom — there's still room for multiple expansion here. The risk: a smaller balance sheet may limit M&A power if consolidation accelerates. Would it crater the thesis? Probably not. For growth-oriented portfolios willing to swing at some volatility, NVT is the speculative, high-upside play on the cooling infrastructure crisis. While everyone's obsessed with compute, smart money is watching what keeps it from burning down.

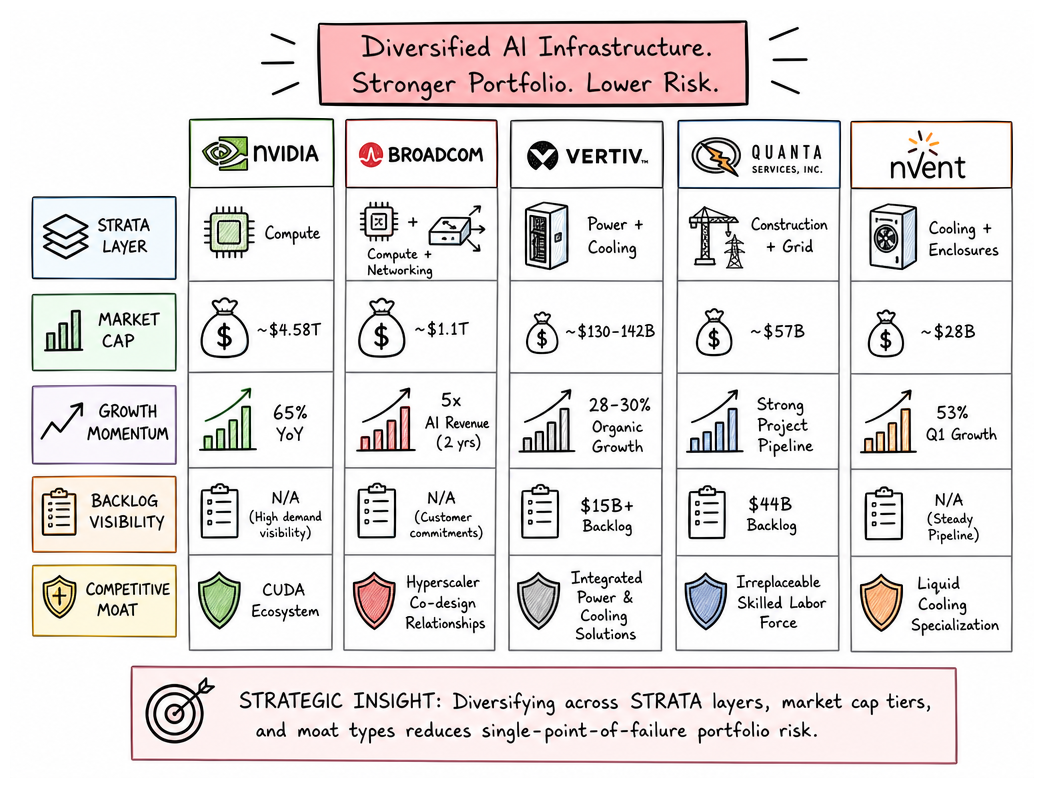

How These Five Stack Up: A Side-by-Side View

Five plays. Five different takes on the same infrastructure bet. Five ways to quickly move heat and electrons off of silicon at levels that make last year's data center look like a toy.

| Company | Segment | Market Cap | Performance | Competitive Edge | Moat Type |

|---|---|---|---|---|---|

| NVDA | Semiconductor Compute | $4.58T | 65% YoY revenue | Sovereign AI + hyperscaler pipeline | CUDA ecosystem lock-in |

| AVGO | Compute + Networking | Large-cap | AI revenue 5× in 2 yrs | Hyperscaler co-design wins | Custom silicon relationships |

| VRT | Power + Cooling | $130–142B | 28–30% organic growth | $15B+ backlog | Thermal architecture expertise |

| PWR | Construction + Grid | Mid-to-large | High single-digit organic | $44B backlog | Irreplaceable field labor |

| NVT | Cooling + Enclosures | $28B | 53% Q1 growth | Strong data center pull | Specialized liquid cooling at scale |

Everyone is chasing NVDA — priced to perfection, with AVGO just behind it. The real money? It's in the plumbing. VRT, PWR, and NVT — the infrastructure layer that doesn't make headlines. That's where margins live. Diversify across layers and single-point-of-failure risk evaporates. You're not betting on one chip vendor losing market share.

Honorable mention: Eaton. Backlog in the data center market hit $19.6B. Eaton acquired Boyd Thermal for grid-to-chip solutions and is working with NVIDIA on 800 VDC architectures. Less pure-play, more diversified — but at the core of the infrastructure enabling the other four.

The Power Demand Problem Nobody Is Talking About

The stack comparison was clean. But the reality everyone is avoiding: compute without power infrastructure is just an expensive bundle of silicon stacked in a warehouse. AI workloads are drawing more electricity than current infrastructure can support. The grid was not designed for this. Load fluctuations are outstripping network capacity — not in the future, but right now.

Fixing that requires a rethink of power infrastructure: rolling higher-voltage (800 VDC) DC power through racks, generating energy onsite rather than depending on the grid, using digital twins to detect load spikes before they impact availability.

Here's where it breaks: deploying new data centers takes years. Permitting. Grid coordination. Construction delays. Enter factory-integrated solutions. With Vertiv's OneCore, deployment time drops by up to 50%. Eaton's Siemens partnership could save up to 2 years on data center construction. Power and cooling bottlenecks are just as investable as compute itself. VRT, NVT, PWR — these are not secondary plays. They're the load-bearing walls.

Speculation, Market Chaos, and the Volatility of AI Infrastructure Stocks

Just because these stocks solve the power problem doesn't make them safe. Macro shocks, tariff headlines, rate moves — they all create violent repricing. These names swing hard. And here's where it gets interesting: the same volatility that punishes passive holders rewards active traders who know how to move.

NVDA, AVGO, VRT, NVT, PWR — they're among the most actively traded infrastructure names in the market. They move fast. For traders hunting alpha in turbulent markets, these STRATA stack companies are prime candidates for both long-term positioning and short-term volatility plays. The infrastructure cycle is real. The power bottleneck is real. But the chaos? That's the opportunity.

What to Watch: Key Catalysts and Risks Through 2026

Catalysts That Matter

- Hyperscaler capex announcements. Every dollar committed to AI infrastructure flows directly into NVDA and AVGO. Real money, committed, with names attached.

- Data center construction awards. PWR's backlog converts to revenue about 12–18 months out. The builder with the longest visibility wins.

- Liquid cooling adoption inflection. Each MW+ rack deployment means NVT and VRT get paid. This is happening now. When pace accelerates, valuations move hard.

Risks That Bite

- NVIDIA export controls. Geopolitical restrictions limiting GPU sales could compress Data Center revenue faster than anyone's model anticipates.

- Custom ASIC acceleration. Meta and Google building their own chips (TPU, XPU) flattens NVDA's growth rate. Market share compression is real.

- Utility grid delays. PWR's $44B backlog shows demand is strong, but project conversion could be stymied by grid bottlenecks.

- Valuation risks for mid-caps. If AI spending disappoints, NVT and similar names could see multiple compression fast.

Honorable mention to watch: Arista Networks (ANET) — $3.5B in AI fabrics revenue projected by 2026 and 90%+ dominance in high-speed switching.

Final Verdict: The STRATA Stack Is a Framework, Not a Trade

Compute doesn't win alone. You can have the fastest chips on earth, but without power flowing in and heat flowing out, your data center is a very expensive, very hot brick. That's the whole premise. Somehow investors keep forgetting it.

These five companies span all four STRATA layers. NVDA and AVGO own compute. VRT and NVT own cooling. PWR owns the construction and grid backbone. None of them win alone. A GPU boom without power and cooling capacity doesn't stall politely — it halts. Full stop.

| Best Fit | Risk Appetite | Why |

|---|---|---|

| $NVDA, $AVGO | Large-cap defensibles | Strong balance sheets, proven moats, cycle visibility |

| $VRT | Balanced defensive | $15B+ backlog, integration moat, compounding gains |

| $PWR, $NVT | Mid-cap upside | Volatile but asymmetric if execution picks up and construction lag compresses |

The execution bottleneck isn't silicon anymore. It's the unglamorous stuff: megawatts, thermal management, fiber runs, concrete poured in the dirt. Each of the five companies here has built a moat, has the balance sheet to survive a downturn, and understands where the current infrastructure breaks. Layered thinking wins. This isn't theory — this is the edge.