The System Stopped Being Honest, So We Built One That Doesn't Have to Be

Fake news in 2016 shook our trust in institutions. In 2024, we feared AI deepfakes. But that's not where the real breakage is. It's deeper. The infrastructure of trust itself — identity verification, content provenance, financial settlement — is collapsing under AI-generated synthetic reality.

The response is more architectural than PR or policy.

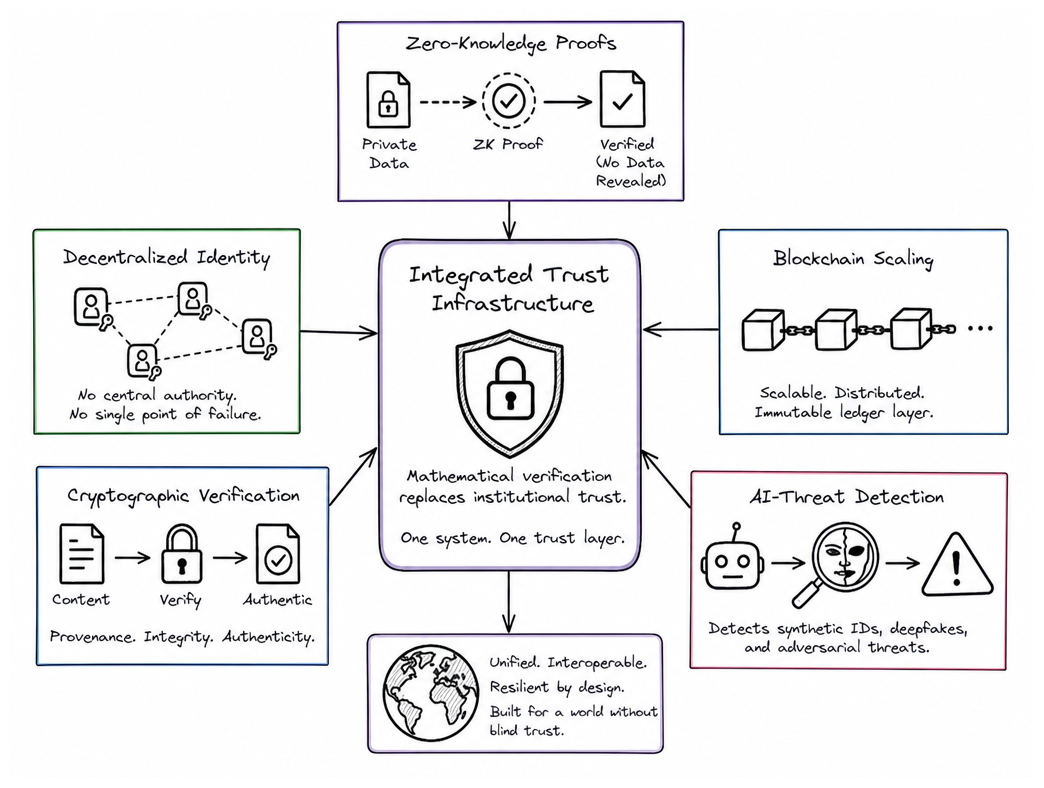

The rebuild:

- Zero-knowledge proofs (ZKPs) — prove something is true without giving away the secret. I can prove to you that I'm over 21 without handing over my birthdate.

- Deepfake detection — cryptographic fingerprints baked into content at the moment of creation. The video, the photo, the article — all carry an unforgeable chain of custody from source to screen.

- Decentralized identity — takes control from trusted institutions and puts it in the hands of the individuals that own it. No more siloed providers. No more single necks to break.

- Blockchain scaling — trustless verification, but at machine speed.

"If the system was honest, why does everything need a zero-knowledge proof?" — It wasn't meant to be trusted forever. It was meant to work until something better showed up. That something is here.

Trust is not coming back. We are replacing it with math. This will be the capital allocation theme of 2026 — not one of, the one. The companies building the cryptographic backbone of verified reality are early. Not venture-stage early. Public-market early. That's the window.

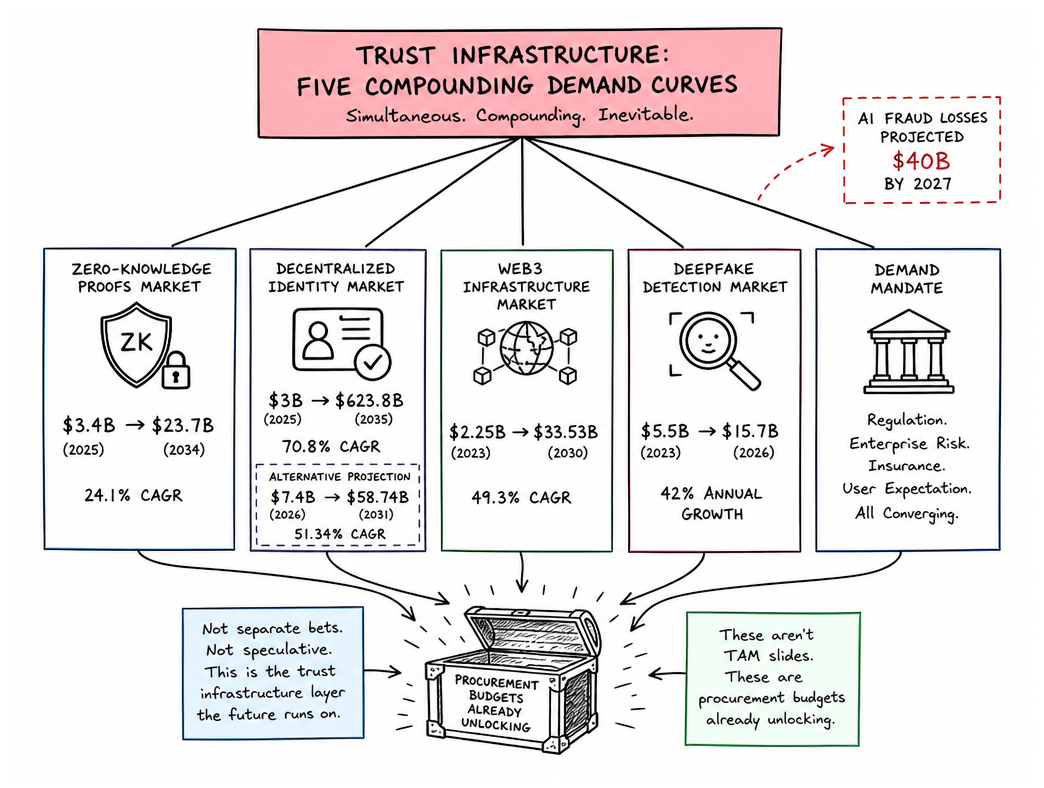

Market Sizing: The Trust Infrastructure Opportunity Is Bigger Than It Looks

Here's what nobody wants to say: this isn't speculative anymore. Demand for cryptographic verification isn't some venture-stage bet. The procurement budgets are already cracking open — whether the market is paying attention or not.

| Market | 2023/2025 Revenue | Future Revenue Potential | CAGR |

|---|---|---|---|

| Zero-Knowledge Proofs | $3.4B | $23.7B by 2034 | 24.1% |

| Decentralized Identity | $3B | $623.8B by 2035 | 70.8% |

| Web3 Infrastructure | $2.25B | $33.53B by 2030 | 49.3% |

| Deepfake Detection | $5.5B | $15.7B by 2026 | 42% annually |

That 70.8% CAGR on decentralized identity — other analyst models also have it at $7.4B in 2026 and $58.74B by 2031 (51.34% CAGR). Either way, the direction is not in question.

When nearly a third of enterprises lose faith in the identity layer, when deepfakes can convincingly impersonate your CEO — that's not a trend. It's an inevitable vendor replacement cycle. Better move now, before the McKinsey slide deck catches up.

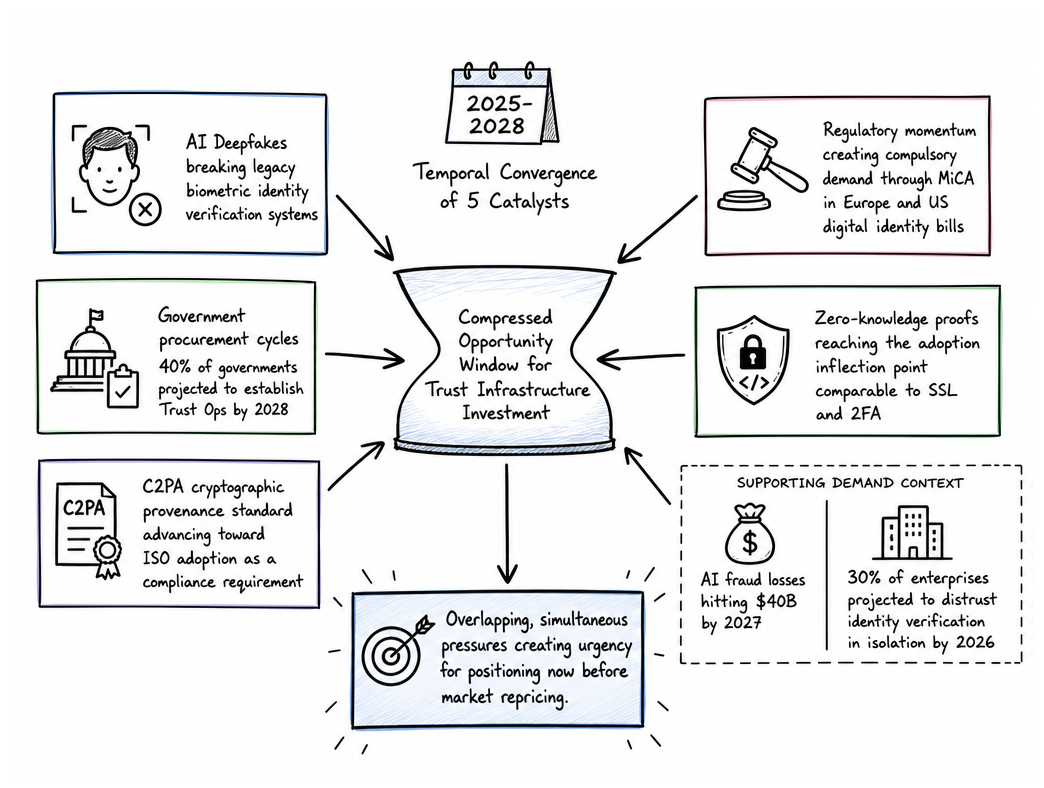

The Catalysts That Make This Theme Actionable Right Now

Everyone knows trust infrastructure is broken. But to do something about it? That's the window — and it's opening right now. Here's what's making acquisition pipelines and government mandates move:

- Legacy biometrics are being nuked by AI deepfakes. By 2026, 30% of enterprises will refuse to use face-based identity verification in isolation — Gartner. The replacement pipeline has to go somewhere.

- Governments are building procurement pipelines. 40% of government organizations will establish "Trust Ops" by 2028 for decentralized identity and synthetic media detection — Gartner, May 2026.

- C2PA moves from differentiator to compliance. The cryptographic provenance standard is on its road to becoming an ISO standard. This is the SSL moment for content authentication.

- ZKPs are entering their SSL/2FA moment. The tech works. The crowd hasn't priced it yet. This is the exact moment that happened with SSL in 2000 and 2FA in 2012 — right before broad enterprise mandates.

Move now, when the tech is proven but no one cares yet. This is the window before the regulators write the memo — before the procurement RFPs go out — before the ETF launches. Windows like this close in a flash.

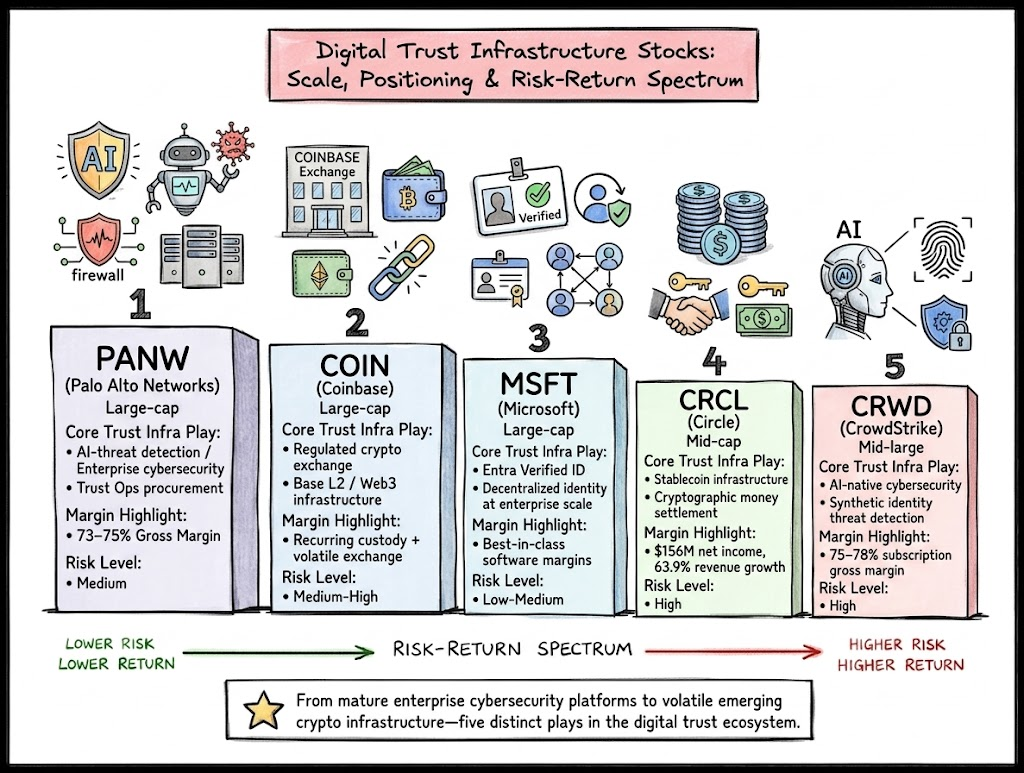

Large-Cap Picks: Palo Alto Networks, Coinbase, and Microsoft

When you bet on large-cap companies early in a theme, you're not betting on invention — you're betting on market position. In trust infrastructure, the early movers already have the enterprise relationships, the compliance certifications, and the platform distribution to absorb this new layer without starting from scratch.

The Deepfake Firewall. PANW's investment thesis is almost boring when you see it all laid out — in the best possible way.

Gross margin of 73.5–75% and FY2025 revenue of $9.2B growing at 14.9%. The biggest moat comes from platform consolidation across Strata, Prisma, and Cortex — a multi-product lock-in that makes switching painful and sticky.

40% of government Trust Operations buildout by 2028 will flow through or be exposed to PANW infrastructure. It's not a point solution. It's a platform that needs to detect deepfake identity attacks and synthetic threat vectors at enterprise scale.

Exchange Fees and Blockchain Infrastructure. Coinbase is not a trading desk. It's building settlement infrastructure underneath regulated Web3.

Recurring revenue streams from staking, custody, and transaction fees from Base mitigate the volatility of exchange fees. USDC is cryptographic verification applied to money — making it auditable, permissioned, and programmable at scale. That's not a stablecoin. That's verified settlement rails.

The brutal truth: every SEC action is a direct event that moves this stock. You have to size accordingly. But the regulated crypto infrastructure narrative is in the final innings of regulatory uncertainty — and Coinbase is the primary beneficiary of what comes next.

The Quiet Infrastructure Play. Microsoft isn't announcing decentralized identity. They're threading it through everything.

Entra Verified ID will be natively woven into Azure and M365 — the enterprise identity stack most organizations already depend on. When enterprises upgrade their identity layer, the path of least resistance runs through Microsoft. Best-in-class software margins with trust infrastructure as a feature layer, not a primary bet.

This is the right play for portfolios that can't stomach pure-play crypto or single-theme cybersecurity concentration. Durable exposure to the theme with enterprise distribution you don't have to build from scratch.

| Ticker | Margin | Primary Risk | Theme Role |

|---|---|---|---|

| PANW | 73.5–75% | Premium valuation; execution risk | Enterprise threat detection |

| COIN | Variable | Regulatory binary risk | Web3 settlement rail |

| MSFT | Best-in-class | Secondary tailwind | Decentralized identity upgrade |

One platform defending against attacks that already broke the old systems. One builder owning the settlement rail few noticed. One quiet giant threading verification into every enterprise login. That's the spread.

Mid/Small-Cap Picks: Circle and CrowdStrike

Now we leave the blue-chip safe harbor and enter the higher-velocity, higher-conviction world — where you're looking for asymmetric return potential, accepting higher volatility in exchange for theme purity.

The Stablecoin Rails Nobody's Talking About. IPO'd on June 5, 2025 at $31/share — $16.7B valuation at close, now valued at ~$31–32B.

Projected 2024 revenue of $1.68B and net income of $156M. Forecasted 2025 revenue of $2.7B (up 63.9% YoY). Q1 2026: $653M reserve income, up 17% YoY; USDC circulation +28%.

Circle went public and no one panicked — which is the whole point. Boring infrastructure moves fast. USDC applies cryptographic verification to money itself — making it auditable, permissioned, and programmable at settlement. The risk: if the Fed cuts hard, reserve income compresses. Also the first public stablecoin issuer means no comparable comp sheet and valuation is still being discovered.

One of the Highest-Beta Pure Plays. GAAP gross margin 75%; subscription margin 78%. That's a software business wearing a cybersecurity costume.

Falcon detects AI-generated threats and synthetic identity attacks at machine speed. No hand-holding. No human in the loop waiting to flag what the model already caught. It's the closest thing to a pure-play AI-native trust verification engine in the public market.

Let's be frank: CRWD trades at a high multiple (78x earnings). It's a momentum name that requires real risk tolerance. It might not be right for every portfolio. But for those who understand that the highest-quality businesses don't discount, this is the one that earns its premium.

Two picks. Different bets on the same collapse of institutional trust. Each with different risk profiles. Size accordingly.

Analyst Verdict: One Thing, Five Ways In, No Hedging

These aren't five unique bets. ZKPs, decentralized identity, blockchain scaling, and cryptographic content verification are all the same structural trade — math replacing trust. Five tickers, one thesis, five different entry points on the risk spectrum.

And now actually use your brain — they're really not hyping up that margin profile:

- MSFT has best-in-class software economics

- CRWD has 78% subscription margins

- PANW is crushing 73–75% gross

- Circle will be posting $156M net income in 2024 alone

This isn't speculative theater. This is real cash compounding while everyone is still debating whether blockchain is really all that important.

Core positions are to be sized around PANW and MSFT. Use COIN as your bridge to regulated crypto infrastructure. Meanwhile, CRCL and CRWD are pure-play asymmetric bets — size them with the risk tolerance they deserve.

These asymmetric windows don't last forever. Early movers see the architecture, while the crowd sees risk. By the time the consensus catches up, the easy money is already gone.

When Dharma Decays, Capital Compounds. In this decade, trust infrastructure will underpin everything. It's not about whether you believe in cryptographic verification. It's about who owns the rails when the world finds out it has no choice.

Recommended Top 5 Listed Trust Infrastructure Stocks

One structural shift. Five tickers. Which do you want to be holding when this gets built?

Stack it how your nerves allow. The architecture gets built in code. Pick your edge.

When Dharma Decays, Capital Compounds.