The Scarcity Trade Is Already Running

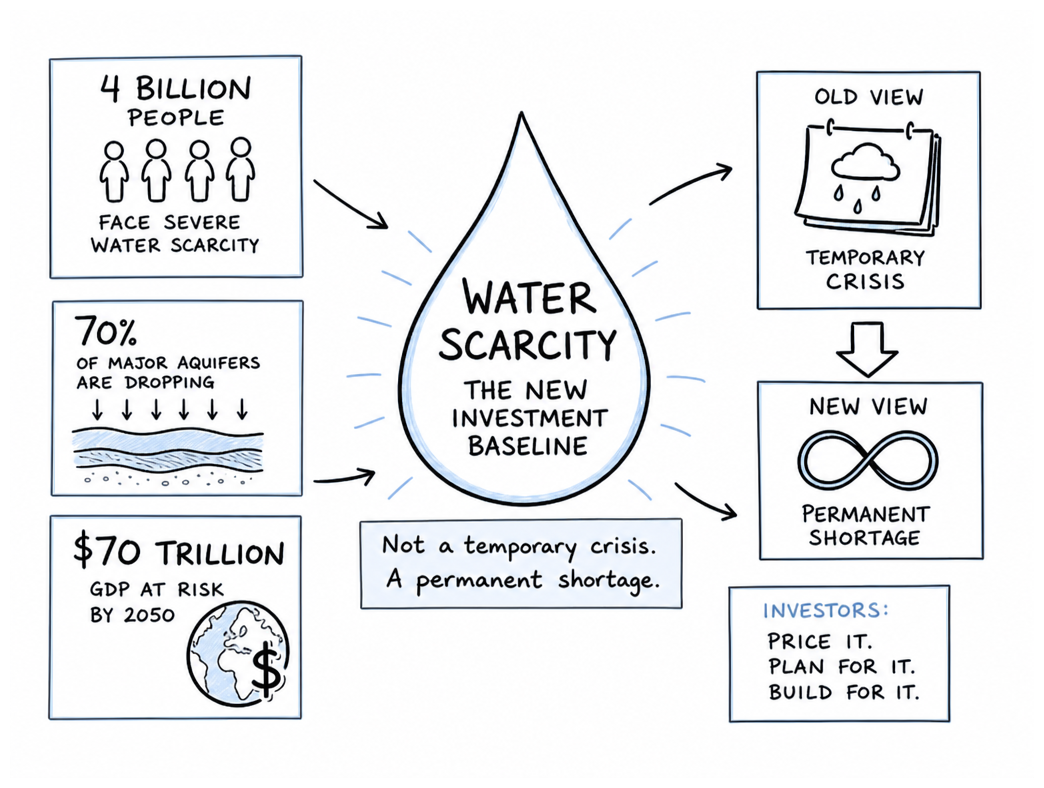

Where you at right now? Because in January 2026, the UN stopped theorizing and called it what it is: global water bankruptcy. Four billion people face severe water scarcity. Aquifers are collapsing. Supply chains for the minerals powering the energy transition are controlled by one country. This isn't a thesis deck gathering dust. It's a capital allocation decision already made.

- 70% of the world's major aquifers are dropping. We're literally sinking the ground beneath 2 billion people.

- More than $70 trillion of global GDP will be impacted by water stress by 2050 — crop collapse, migration, factory closures.

- Droughts already cost $307 billion annually — and this number compounds.

If a crisis is temporary, you hedge, endure it, and it ends. If you are faced with a permanent shortage, you own the infrastructure that manages it. That's not speculation. That's what institutional capital is already doing.

Water infrastructure stocks, critical mineral processors, uranium producers — these aren't niche plays. They're structural. The scarcity trade is running whether you're positioned or not.

Why These Markets Demand Attention in 2026

Has the market fully priced what's structural here? Because the gap between what's priced and what's locked in is still wide enough to drive a truck through.

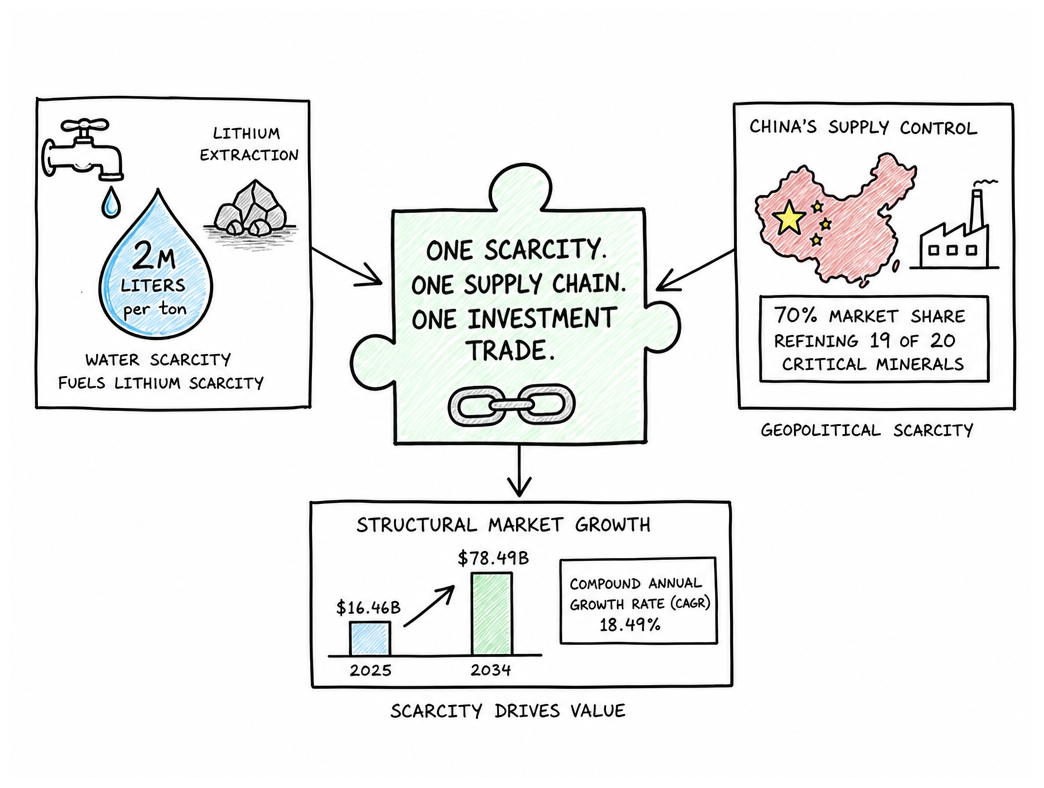

The water math is brutal: Droughts already cost $307 billion a year. Hedge funds aren't waiting on policy — they're actively buying up aquifers. Greenstone flipped Colorado River water rights for a reported 15x return. This isn't speculation. This is money that's done the math and decided the shortage is locked in.

On the lithium front, Fortune Business Insights sees the opportunity at $16.46 billion in 2025 growing to $78.49 billion by 2034. The kicker: lithium extraction uses around 2 million liters of water per ton. The scarcity of water and the scarcity of critical minerals are the same trade wearing different clothes.

Critical minerals are defined by supply risk and economic necessity. Once the supply chain is locked, they compound fast. The US response — Defense Production Act, DoD equity stakes, offtake guarantees — is already creating government-backstopped scarcity plays in the public markets.

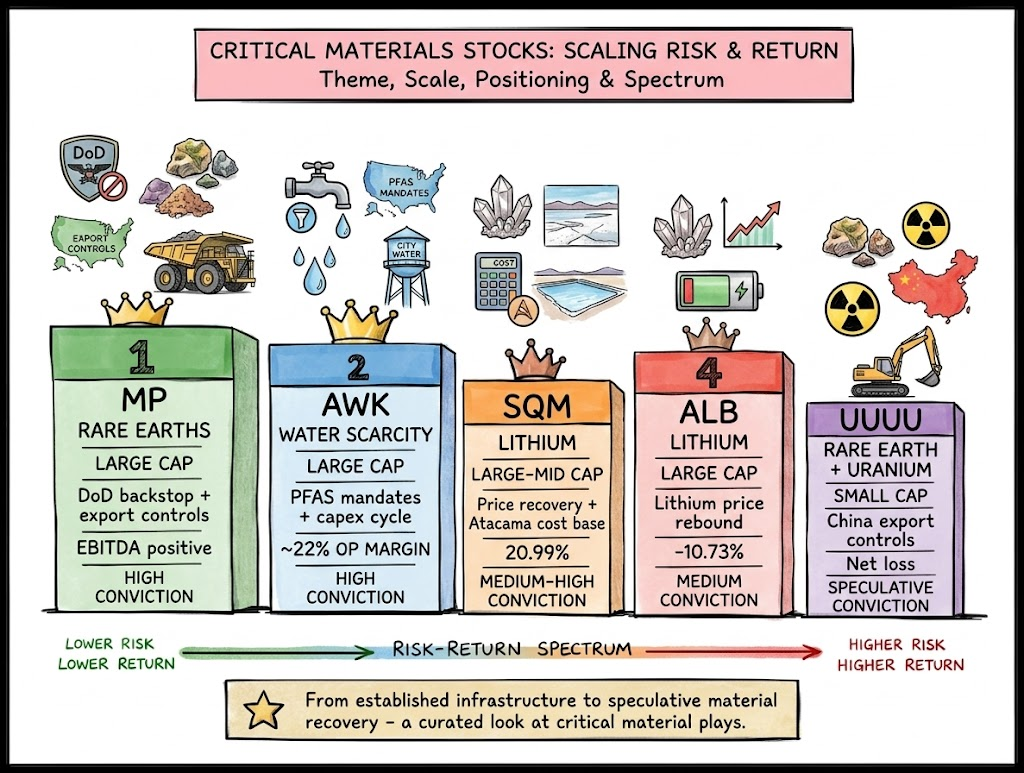

Large-Cap Pick #1 — American Water Works (AWK)

Forget buying up aquifers — the best and most reliable play on water scarcity may be to own the pipes everyone has to use. AWK is the largest publicly traded US water and wastewater utility. The regulated utility model is where the magic lives: no matter the macro chaos, AWK just keeps billing.

Own the Pipes. The largest publicly traded US water utility — 14 million customers across regulated service territories. The regulatory moat is deep: rate cases lock in revenue regardless of market conditions.

IIJA funding unlocks new capital, EPA PFAS rules force hard spending on treatment upgrades (which become rate base), and every new home built in a service territory adds a customer forever. The squeeze: rising rates compress utility valuations, and regulatory approvals can get complicated by political uncertainty. But the structural demand doesn't care about any of that.

Large-Cap Pick #2 — MP Materials (MP)

The Only Rare Earth Mine That Matters. MP runs the only active large-scale rare earth mine in the US — Mountain Pass, California. The DoD gave them $400M in equity and a $110/kg price floor on neodymium-praseodymium. They're literally betting their defense supply chain on this mine not failing.

China's ramping up its rare earth export restrictions and never seems to stop. Mountain Pass is winning by default. When the government is your largest shareholder and your price is guaranteed by national security imperatives, you're not looking at a stock anymore. You're looking at a government-sponsored monopoly on domestic rare earth supply.

Large-Cap Pick #3 — Albemarle Corporation (ALB)

The Cyclical Recovery Bet. When you're the world's biggest lithium miner and your margins turn underwater, do you panic or view it as a fire sale on the dominant player in a permanent-demand commodity?

Lithium companies will eventually benefit from rising lithium prices — and when that happens, Albemarle's scale gives it the highest operating leverage in the sector. 52-week range of $53.70–$221.00 tells you everything about where we are in the cycle. This is not a stock for the faint-hearted. It's a bet that the lithium cycle turns, and the biggest player captures the most.

Mid-Cap Pick #4 — SQM (NYSE: SQM)

Margin Floor That Doesn't Flinch. Albemarle is the cyclical recovery bet. SQM is different — through the entire lithium downcycle, SQM has maintained a 20.99% operating margin. Not the peak. The floor. If lithium prices get back to range, the upside is asymmetric.

Here's the rub: Santiago could nationalize the whole operation. Chilean government contract renegotiation is live. Lithium nationalism is real and the sovereign risk is priced in — but not fully. For investors with the stomach for geopolitical risk, the margin profile is extraordinary. This is a high-conviction bet on lithium recovery with a built-in political risk premium.

Small-Cap Pick #5 — Energy Fuels (NYSE American: UUUU)

The Dual-Commodity Speculative Beast. If you want speculative exposure to the geopolitical knife fight over rare earths AND uranium simultaneously, here it is. US-listed, dual-commodity exposure — uranium and rare earths in the same vehicle.

Currently running a net loss — that's what makes it speculative. But dual exposure to two of the most geopolitically charged commodities on the planet means the upside in a shock scenario is violent. Chaos is the asset class. 52-week range of $4.82–$27.90 tells you this is a high-beta ride. Size it accordingly.

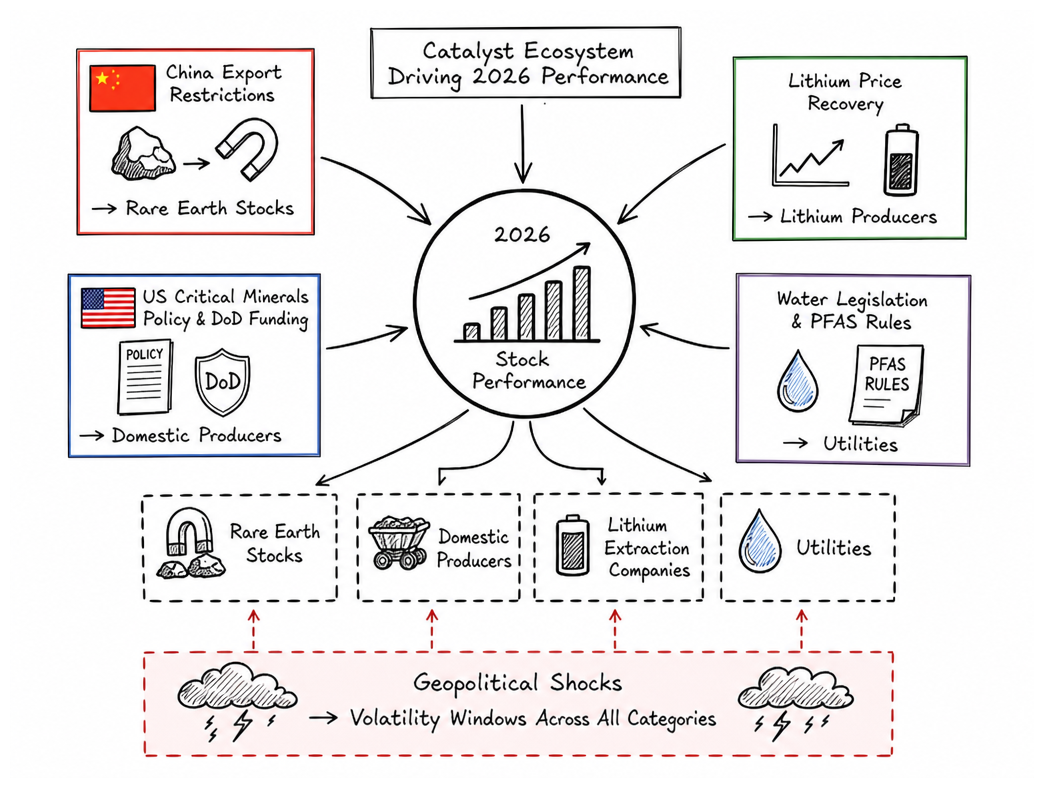

Catalyst Map — What's Driving These Stocks in 2026

What actually triggers repricing in scarcity plays? Shocks. Not patience.

- China export restrictions escalate. Any rare earth embargo screams across the sector. One move from Beijing and you get immediate violent repricing in MP and UUUU.

- US critical minerals policy tightens. DoD dumps capital into domestic capacity. DPA Title III funding and executive orders locking supply chains directly backstop MP and UUUU valuations.

- Lithium prices start to rise again. Spot price crawling back from the 2024–2025 trap triggers operating leverage in ALB and SQM. EV demand is structural, not cyclical.

- Water legislation accelerates capex. EPA-mandated PFAS standards and rate-base increases flow directly into AWK's regulated revenue model.

- Institutional capital enters water rights at scale. Smart money buys. Retail notices. The re-rating does the rest.

Geopolitical shocks create speculative windows. The real money flows to whoever's positioned before the narrative locks. The degen trader community at kalyugcapital.com is built around exactly this edge — Kalyug, the age of accelerated decay, means the windows open fast and close faster.

Ranked Summary: Top 5 Vital Extract Stocks for 2026

When scarcity starts pricing in, which five stocks will actually matter? Ranked by government backstop, margin durability, and asymmetric upside:

1. MP Materials (MP) — DoD gave them $400M in equity and a $110/kg price floor. This isn't a stock. It's a government-sponsored monopoly on domestic rare earth supply. Highest conviction in the theme.

2. American Water Works (AWK) — $5.14B revenue, $3.7B capex locked through 2026. Regulatory margin ~22%. As steady and boring as it gets — which is exactly what scarcity infrastructure looks like at scale.

3. SQM — 20.99% operating margin through the downcycle floor. If lithium prices bounce, the upside is asymmetric. Geopolitical risk priced in but not fully.

4. Albemarle (ALB) — Largest lithium player means highest operating leverage on price recovery. Down hard — which is also what makes it interesting. This is the cyclical bet, not the defensive one.

5. Energy Fuels (UUUU) — Dual uranium and rare earth exposure. Net loss now, violent upside in a shock scenario. Chaos is the asset class. Size it with the risk tolerance it deserves.

Scarcity isn't a trend. It's the baseline now. Alpha comes from positioning before the market locks the narrative down.

When Dharma Decays, Capital Compounds.