The Price of Free Things

Water is free. Legally, in many places in the U.S., water is a public good — (near) free at the tap. And yet institutional capital is moving into water rights like it's the last frontier of extraction. That's where the gap comes from. That's the whole trade.

- Zero price meets infinite necessity. That's where scarcity trades breed. The spread between "free" and "I will die without this" is where the money lives. Full stop.

- No institutional investor buys something that isn't going to rise. If hedge funds are buying thousands of acres based on the aquifers beneath them, they've done the math. You just haven't seen it yet.

- This isn't some niche thing. This is a structural macro trade. It's going to determine how the world distributes its most important resource.

Let's call this Vital Extract: the real and valuable things that literally underpin modern life. Water is the prime example — but the same bottleneck thinking applies to clean energy inputs, lithium, phosphorus, rare earths. Different commodities. Same chokehold.

We just entered global water bankruptcy. That's not metaphor. That's the new baseline.

Global Water Bankruptcy — A Clinical Reality

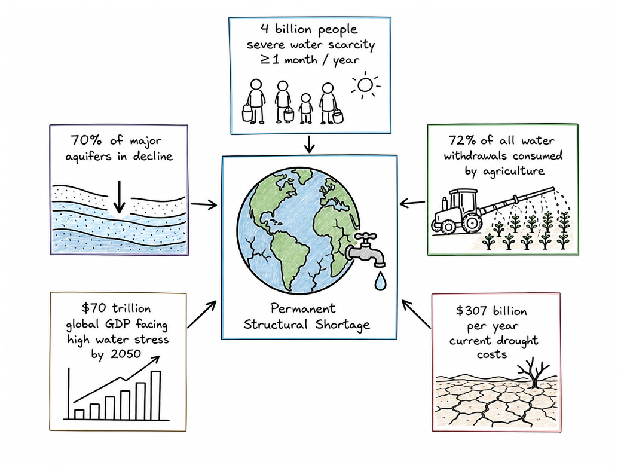

In January 2026, the UN stopped sugarcoating and started calling it what it is: global water bankruptcy. Four billion people now face severe water scarcity for at least one month per year. It's not a risk. It's not a headline. It's a new normal.

70% of major aquifers are dropping. 72% of water withdrawals go to agriculture — and a big portion is wasted. Climate change shows up: rising temps, unpredictable rainfall, drought after drought. We're literally sinking the ground beneath 2 billion people due to groundwater depletion.

By 2050, high water stress will impact up to $70 trillion in the world's GDP — crop collapse, migration, factories closing. Droughts are already costing $307 billion annually. And that number compounds.

Temporary crisis = you hedge, endure, and it ends. Permanent shortage = you price to the scarcity as your baseline. You don't ask if it gets worse. You assume it will.

Here's when the real money comes in. Institutional money. Money that calculates regulatory risk, has strong conviction, and doesn't falter under local outcry. Because once scarcity becomes structural — once everyone agrees the shortage is permanent — value extraction becomes the only game left to play.

Water's going to be owned by somebody. The question isn't if. It's who — and how far they'll go to keep it.

Hedge Funds Don't Buy Things That Aren't Going Up

So the smart money decided water is an asset class. Not farmland. Not infrastructure. Water. Full stop.

Water Asset Management — a New York City hedge fund — dropped $100 million cash on 12,793 acres in Arizona's McMullen Valley. The dirt was window dressing. Arizona's Attorney General started asking uncomfortable questions about whether that groundwater was headed for export to Phoenix. Local officials raised alarms. Residents fought back. The fund kept buying.

Same playbook. Different geography. Colorado's Grand Valley: over $6.2 million for water rights on roughly 800 acres, with plans to scoop up 2,500 total. Land acquisition? Cover story. The water entitlements were the prize.

Then there's Greenstone Resource Partners. Bought 485 acres of farmland for $9.8 million. Sold the water entitlements — 2,033 acre-feet of Colorado River allocation — for $24 million. Fourteen million dollar gross profit on a legal fiction. The farmland was a wrapper. Everything else was theater.

| Case | Purchase | Price | The Real Asset |

|---|---|---|---|

| Water Asset Management (AZ) | 12,793 acres | $100M | Groundwater rights |

| Water Asset Management (CO) | 800–2,500 acres | $6.2M+ | Water entitlements |

| Greenstone Resource Partners | 485 acres farmland | $9.8M | Colorado River water ($24M resold) |

When scarcity becomes structural, arbitrage becomes obvious. Critics use words like speculators and vultures. The funds call it a "trillion-dollar market opportunity." Both are describing the same thing — just with different moral weight.

Colorado has anti-speculation laws on the books. Beneficial use requirements. Restrictions on out-of-state transfers. Good laws. Problem is enforcement melts under pressure. When rules become suggestions and litigation costs spike, the vultures circle tighter. This isn't investment anymore. It's extraction wearing a legal suit.

The Clean Energy Trap: You Can't Build Green Without Destroying Water

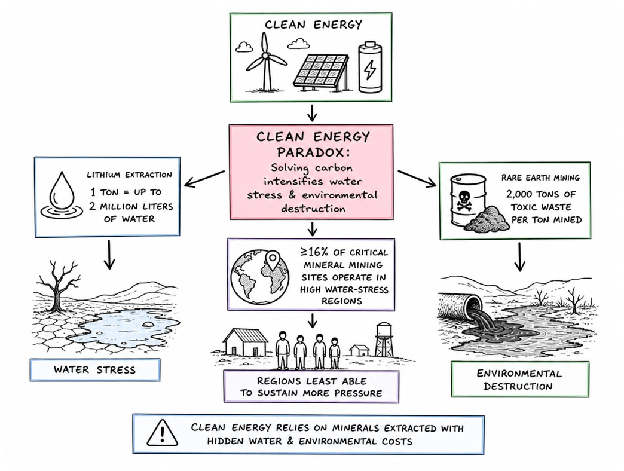

Here's the unspoken truth: saving the planet is an inherently resource-intensive task. We need enormous amounts of raw materials — cobalt, copper, lithium, and rare earths for the grid, EV batteries, and wind turbines. These metals are central to the energy transition. Without them, it comes to a screeching halt.

Rare earth stocks and critical mineral infrastructure are now priced as a structural fix for fossil fuels — an asset class pulling serious institutional money, betting that you can engineer your way through the contradiction baked into the whole scheme.

But here's the contradiction:

- Lithium extraction in the Lithium Triangle consumes up to 2 million liters of water per ton. Aquifers are being drained, communities downstream are left with nothing, and drinking water gets poisoned.

- For every ton of rare earth mined, 2,000 tons of toxic waste are generated — some of it radioactive waste that'll stay buried in the ground permanently. Permanent land damage that no government has budgeted to clean up.

- At least 16% of critical mineral mining sites already operate in high water-stress regions. We're mining critical minerals in places already facing water scarcity.

You're putting out one fire by torching another. Trading carbon for water. Trading greenhouse gases for radioactive tailings. One type of planetary exhaustion for another.

The bottlenecks aren't in a marketing deck. They're in the ground. They're finite. They're contested. And they're controlled by players you haven't thought about yet.

Rare Earths and the Geopolitical Chokehold

So we dig up the minerals. Extract them. And then what? There's a gatekeeper standing in the way — holding the entire transition hostage.

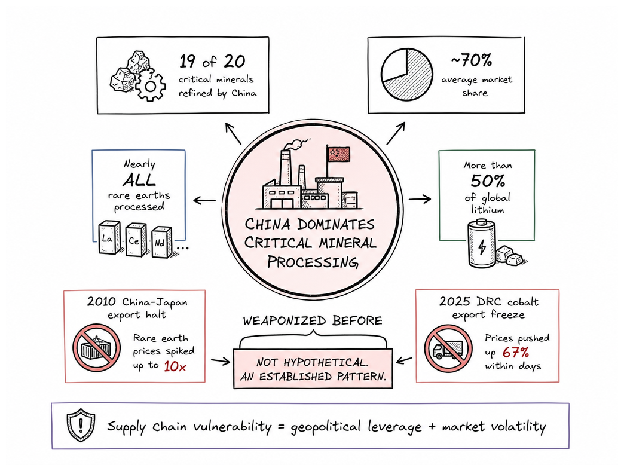

19 out of 20 critical minerals have China as the dominant refiner, with an average market share of around 70%. China refines almost all rare earth elements, two-thirds of cobalt, and over half the world's lithium. That's not just a supply chain. That's a chokehold with extra steps.

Supply chain vulnerability isn't theoretical. It's weaponized. In 2010, China halted rare earth exports to Japan over a fishing dispute. Prices spiked 10x in days — from a political tantrum. Fast-forward to 2025: the DRC's four-month cobalt export lockdown pushed prices up 67% within days. The pattern repeats. The vulnerability compounds. Each disruption becomes a template for the next one.

Fundamentals don't move rare earth stocks. Instead, they move on shock — geopolitical shock, supply shock, the moment some official sneezes in Beijing or Kinshasa and the entire trade flips. It's a commodity play, but very much a volatility machine the market knows quite well:

- Concentration risk is now a feature. Institutional capital isn't pricing stability — it's pricing the next disruption.

- Precedent gets weaponized faster each cycle. Every freeze becomes a playbook for the next regime.

Vital Extract: How to Think About Long-Duration Resource Constraints

Here's what really matters: it's not in the price swings. It's in the immobility. You can't print water. You can't suddenly substitute rare earths once the supply chain locks. You can't offshore lithium. They sit where they sit — and that's where the asymmetry lives.

The Vital Extract thesis breaks down simply: some commodities can't be replaced, printed, or moved, they're geographically bound, and demand is rising. Here's why each one is an isolated trap:

- Water — Legal ambiguity plus physical scarcity equals positioning for institutional players willing to wait. While regulators have concerns over "water speculation," the law hasn't addressed the ambiguity. Patient capital is snapping up aquifers while the system tries to figure things out.

- Rare earths — China processes 19 of 20 critical minerals with ~70% total market share. Extreme processing concentration plus rising clean energy demand equals perpetual supply shock risk. Concentration isn't a feature. It's a vulnerability we all agreed to live with.

- Lithium — Up to 2 million liters of water to extract a single ton. That embedded water destruction already represents unpriced regulatory and social risk. It will be priced in soon.

- Indigenous land conflict — 54% of energy transition mineral projects sit on or near indigenous lands. Governance isn't a footnote — it's a wildcard that can freeze entire supply chains overnight without warning.

Long-duration resource trades have one thing in common: they look boring until they don't. Then they look inevitable.

The quiet money is already here, waiting. Speculative opportunities are quietly compounding before they explode into narratives everyone suddenly pretends they saw coming. You're watching the early innings play out.

Chaos Is the Asset Class

Resource constraints — water shortages, squeezed clean-energy inputs, rare earth supply shocks — all generate volatility. Volatility is tradeable.

Patient capital buys the aquifer. Aggressive capital trades the shock.

Who's on the wrong side of this trade? Most of the market. Long-duration resource shocks cause enough turbulence to separate people prepping for the chaos from those caught in it. Water rights move slowly, then rare earth prices seize, then spike — and everyone acts shocked, as if the price was never wrong.

The aquifer is bought by patient capital. Aggressive capital trades the moment when everyone realizes they've been holding the wrong end of the knife all along.

The Scarcity Trade Has Already Started

It isn't coming. It's already here. Institutional money has stopped theorizing and started buying — water rights, critical minerals, extraction assets, all of it. Silently, thousands of acres are being bought by Wall Street firms who've captured a future where these assets don't just increase in value — they're essential.

The public finds out through lawsuits and legislation. By then the position is locked. Arizona's farmers will scream about groundwater exports. Senators will wake up to how essential rare earths have become. Meanwhile the volatility you see? Surface noise. The real move is structural and patient.

Water infrastructure stocks — utilities, treatment facilities, desalination plays — let ordinary capital gain exposure to the same thesis without buying 13,000 acres in the desert. The question isn't whether resource scarcity will matter. The question is whether you're on the right side of it when it does.

When Dharma Decays, Capital Compounds.